Cathie Wood. Her firm’s funds have struggled lately, but that’s normal in her space. The simple fact is that many of the technologies and companies she invested in became their own bubbles. Anyone remember Amazon or Microsoft in 2001? But great buying opportunities. I don’t think we are there quite yet, but when the Fed hopefully kills the inflation monster, those tech stocks will be the Amazons and Apples of the future.

Cathie looks for innovation because that’s what solves problems. Innovation is inherently risky. Sometimes the solutions don’t work, or you need a long time to make them work. Impatient investors don’t like that part, but it goes with the territory.

Cathie talked about three top problems she thinks technology is ready to solve: inflation, energy, and supply chains. These solutions will help countries become more resilient and less vulnerable to these global contagions. She pointed out that innovative solutions are, by definition, different from the current standards. That draws criticism, but it’s also what makes them work.

Tesla, for instance, started out doing something new with electric vehicles. The automotive industry’s vast supply chains weren’t set up to do what Tesla needed. This forced the company to become vertically integrated—something business schools usually say is a terrible mistake. Tesla had to bring almost everything in house, at least in its early days. That’s been costly, but now it makes the company less dependent on outside suppliers. That is allowing it to expand quickly while much larger, global brands race to catch up.

Ed D’Agostino, who was interviewing Cathie, pushed her on that point. He said US equity markets don’t like vertical integration, and it often draws in activist investors who push for change. Here is Cathie’s response.

This is the way innovation often evolves. If you look at the early days of cell phone manufacturing, for example, I think many people are surprised to learn that Qualcomm felt compelled to build its own phones because it wanted to speed up adoption, and nobody believed that cell phones were going to take off the way they did. Tesla had to do the same thing. And we’ve talked to Tesla about this. You know, the cell phone industry, of course, evolved so that it wasn’t so vertically integrated after all. And I do think Tesla is thinking that with time, as supply chains become more, shall I say, commoditized, it probably will move away from verticalization.

But there’s one thing that could prevent it and which would present it with an incredible barrier to entry, and that is if Tesla is successful at evolving the first national autonomous taxi platform, it will have done so because of its AI chip—artificial intelligence chip–this is the equivalent of Apple designing its own chip for smartphones because nobody thought of that or believed smartphones could happen. Apple redefined the industry.

Tesla’s doing the same in the transportation industry with autonomous, and what we’re finding out with the use of artificial intelligence and given the importance of safety when you’re talking about autonomous driving, you have to titrate the cars very carefully using the data and all of the sensors. It’s a very delicate balance, and it changes from car model to car model. So we think that these years of vertical integration could extend if Tesla becomes successful in the autonomous taxi platform market.

Again, this is something with macro consequences if correct. Millions of driver jobs—taxis, delivery vehicles, long-haul trucks, and more—are at stake. Can Tesla develop chips that will push goods through the economy more efficiently than human drivers? I think we will find out. And if it’s not Tesla, it will be someone else.

Cathie went on to talk about technology and “precision agriculture” solving many of our food challenges. Intelligent farm equipment can increase crop yields while using less fuel, fertilizer, and other inputs.

The automotive industry is racing to make the economy’s circulatory system work better, eliminating arterial blockages and helping “nutrients” flow better. Meanwhile, the agriculture industry is using technology to expand the supply of nutrients that keep us healthy.

US Economy

- The U. Michigan consumer sentiment index dropped to the lowest level since 2011, as gas prices hit record highs.

- These levels of consumer sentiment look recessionary. Here are some trends from the U. Michigan report.

- Current financial conditions:

- Expected longer-term income gains:

- Expected business conditions:

- Buying conditions for durables:

- Buying conditions for houses:

- Freight rate inflation has been unprecedented but it appears to be peaking.

- Freight trucking shortages are easing.

- Outside of vehicles and a few one-off items, retail inventories have improved markedly.

- Consensus forecasts for 2022 show rising stagflationary risks as economists rapidly downgrade the GDP growth projections.

- The market-based probability of a 75 bps Fed rate hike in June is now below 10%.

- Tighter monetary conditions have been a tailwind for the US dollar.

- The NY Fed’s manufacturing index (the first regional report of the month) surprised to the downside.

- This report doesn’t bode well for manufacturing activity at the national level (ISM).

- Demand appears to have slowed.

- And backlogs are rapidly easing.

- Price expectations seem to have peaked

- Bloomberg’s economic/cycle surprise index has been deteriorating.

- US retail sales held up well last month despite inflationary pressures. At least for now, the US consumer has not retreated.

- Industrial production topped expectations, as the nation’s manufacturing output keeps climbing.

- Manufacturing capacity utilization is at multi-year highs.

- The Atlanta Fed’s GDP growth model estimate for Q2 moved higher in response to the economic reports above.

- Business inventories continued to climb rapidly in March.

- Homebuilder optimism slumped this month, with housing sales expectations tumbling

- Single-family housing rental costs are up substantially over the past 12 months.

- Air travel is improving, albeit still below 2019 levels.

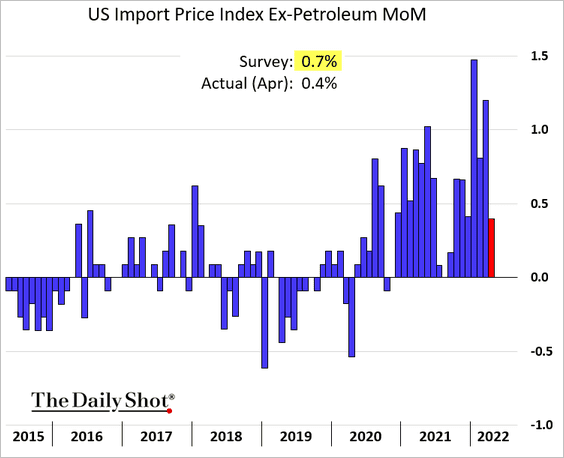

- The recent strength in the US dollar (below) has slowed import price gains.

- For now, high-frequency indicators point to a slowdown, not a recession.

- Mortgage applications to purchase a home and rate locks declined sharply last week.

- The fastest increase in mortgage rates in decades and rapid gains in housing prices have been pressuring affordability.

- And it’s finally starting to take a toll on housing demand. The stock market rout is also raising concerns about housing.

- Refi activity continues to shrink.

- Active home listings are no longer falling.

- Housing starts were strong last month, boosted by apartment construction

- But permits softened.

- Construction backlogs persist.

- Here are the industries with the highest labor shortages among small businesses.

- Wage growth decelerated recently.

- Private capital flows into the US have been surging, providing support for the dollar.

- US gasoline demand has strengthened.

- Similar to the NY Fed’s manufacturing report, the Philly Fed’s regional factory activity gauge surprised to the downside.

- While current demand appears to be robust,the outlook index hit the lowest level since the financial crisis.

- Supplier delivery times are off the peak but still elevated.

- And cost pressures persist.

- However, manufacturers overwhelmingly expect supply bottlenecks to ease over the next six months.

- The CapEx expectations index hit the lowest level since 2016.

- Are we facing an inventory glut? The Philly Fed’s forward-looking indicators (above) suggest that it’s a possibility.

- US job openings have peaked. Job postings on Indeed have been drifting lower.

- Revelio’s data also points to a decline in job postings.

- Conference Board’s leading indicator unexpectedly declined last month.

- Existing home sales were soft last month, down almost 10% from 2021.

- Weaker mortgage applications and higher mortgage rates point to further weakness in existing home sales

- Existing home inventories are still very low but are rising faster than usual for this time of the year.

- Weak homebuilder sentiment also points to declines in residential construction.

Market Data

- Outside of a recession, equities tend to recover after bearish sentiment reaches an extreme (2 charts).

Source: @hedgopia

Source: Evercore ISI Research

- Historically, high inflation and rising yields have been a headwind for equities. But are we shifting to the “high inflation and falling yields” regime?

- The consensus forward earnings for the S&P500, S&P400, and S&P600 are pointing to robust profits growth over the coming year. Are analysts too optimistic?

Source: Yardeni Research

- Goldman cut its S&P 500 2022 year-end target from 4,700 to 4,300.

- Some of the most expensive stocks have seen the worst returns so far this year.

- US equities’ relative performance has diverged from the US dollar.

- Small caps continue to trade at a deep discount to large caps.

- Fund managers are extremely bearish, according to BofA.

- Cash levels:

- Corporate earnings are facing significant headwinds.

- Fund managers haven’t been this gloomy about corporate profits since 2008.

- Bear market underperformers tend to outperform on the rebound.

- Which are the world’s cheapest and most expensive currencies?

Quote of the Week

“Forgiveness does not change the past but it does enlarge the future.”

Picture of the Week

All content is the opinion of Brian J. Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}