My friend Dan has extensive experience in the CRE world—including with all property types and in all market conditions—having worked on over 800 transactions with a total value exceeding $26.3 billion, spanning development, ownership, repositioning, restructuring, and lending. Commercial Observer recognized him as one of “The Most Important Figures of Commercial Real Estate Finance.”

Dan believes that with the tumultuous state of the commercial real estate market, investors should seek protected risk-adjusted returns, which is what we do with our two-sided strategy.

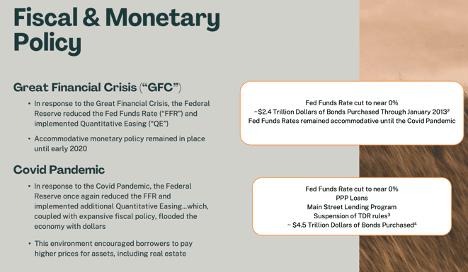

Below are a few slides that sets the stage. It’s information you know, but it’s always good to review:

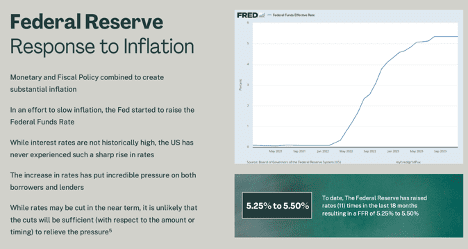

The key is the last statement: “This environment encouraged borrowers to pay higher prices for assets, including real estate.”

Inflation followed: “The increase in rates has put incredible pressure on both borrowers and lenders.”

Perhaps the most telling slide in Dan’s presentation is this next slide.

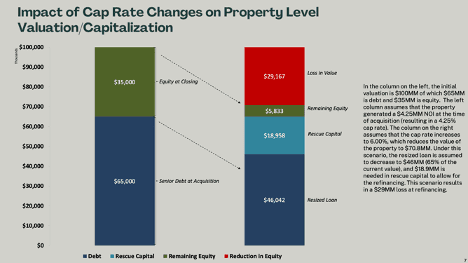

Here are the basics:

- Deals were done where the asset buyer put up 35% of the equity, and the bank financed the remaining 65%. That’s 65% debt to 35% equity.

- At the time of the acquisition, the property generated $4.25 million (net operating income).

- But now, since financing costs have increased so much, the net operating income generated from property rents has decreased. In the case of commercial office space where we have high vacancies, it’s even worse.

- So, the value of the building is now worth less.

- The challenges come when the buyers need to refinance the loans.

- The bar on the right in the graph below assumes the cap rate increases to 6%, which reduces the value of the property from $100 million to $70.8 million.

- Under this scenario, the bank will resize the loan to $46 million, down from $65 million.

- As a result, the property owner will lose $29 million, so they need to find some rescue capital in order for a new loan to be written.

- This assumes the property owner is earning enough in rental income to cover expenses, including the higher interest costs.

- Without rescue capital, the owner turns the keys over to the bank.

- Thus, “jingle mail.”

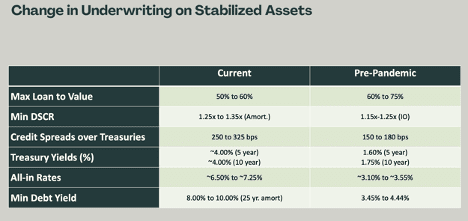

The cost of borrowing has risen sharply. In the chart below, look at the change from pre-pandemic levels to current ones.

One popular REIT (real estate investment trust) fund needs a 180-bps decline in the Fed Funds rate. Otherwise, they’ll have to eliminate their entire dividend payout.

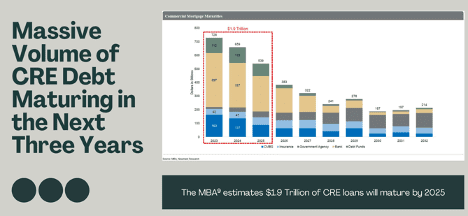

See the debt maturity calendar below (squared in dotted red). The tipping point is when the loans mature and need to be refunded. Dan said the 2023 loans have been pushed to 2024, which, surprisingly, the banking regulators are allowing for now. Pretend and extend, apparently. Everyone is hoping the Fed will cut rates by six times or more.

But there is a short timeline for the ability to avoid the issues; there’s $1.9 trillion due to be refinanced.

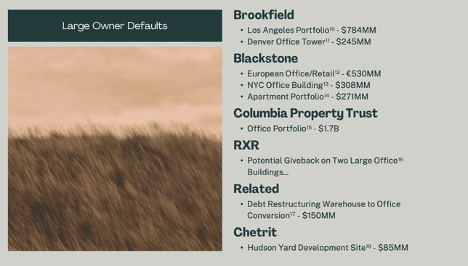

Many large owners have already started defaulting on their properties. And several more have happened since Dan created this slide.

For his own part, Dan previously owned 36 properties. He sold them all a few years ago and is waiting to reenter the market to buy at distressed prices. According to him, there’s no reason to go over the top and buy these assets right now because every banker he talks to says they “have no problems,” but the loans paint a different picture. He says he’s made offers, and they go to their board of directors or board and waive all the covenants. But you shouldn’t be able to do that if you’re an SEC-reporting bank and you’ve got to issue GAAP-compliant statements. This tells us that the Feds have softened their regulatory position (for now). If Dan were still Vice Chairman of a bank, they would have made him reappraise and take write-downs on every single asset.

Dan is concerned that the Fed will create a Bank Term Funding Program number two similar to the BTFP they created on March 12, 2023, in response to the banking crisis (SVB, Signature Bank, etc), except that this time, they’d allow banks to push off their bad commercial real estate loans at par.

Dan suggested that another possible solution, modeled after something utilized in Europe, that doesn’t involve another government bailout. Europe created a market for synthetic securitizations based on Basil III banking standards that allow you to make what is called a substitution. It involves getting a guarantee from another entity that can issue debt. Think of outside investors putting capital into various pools of different levels of risk-and-reward investment structures. This new capital shifts the risk, allowing the banks to free up capital in their books.

The challenge is that no banking regulator is currently willing to give Dan and his team an opinion on this. They will only give their opinion directly to a bank. I’m pulling for Dan.

Concluding thoughts:

Capital will freeze up in another banking crisis. I believe that the Fed is well aware of the problem, and they’ve certainly shown the will to backstop the system with creative new programs. Dan concluded that we were at the top of the first inning with the first batter at the plate—still early in what is likely to be a big problem unless the Fed takes the Fed Funds rate back down to 3% (my guess) or creates something similar to the Bassel III enabled synthetic market in Europe. However, I really have to learn more about that market. A better solution at face value than putting more junk assets, priced at par, but worth significantly less, onto the backs of the US taxpayers.

Electric Vehicle Companies

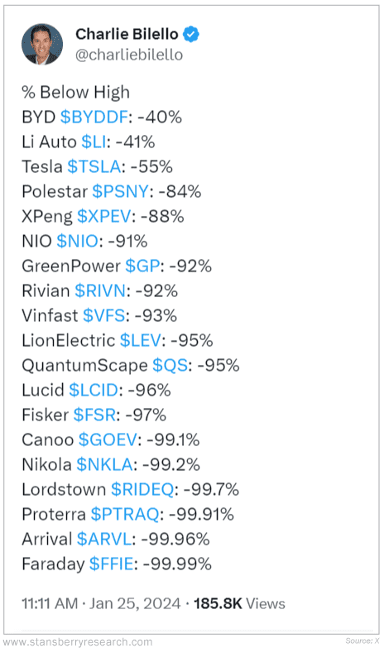

Number-cruncher extraordinaire Charlie Bilello recently posted on X (formerly Twitter) a list of 18 EV manufacturers and one battery maker trading anywhere from 40% to 99.99% below their all-time highs.

Only three of the companies –Tesla (TSLA) and China-based BYD (BYDDF) and Li Auto (LI) – report any profits at all, and they’re all trading 40% or more below their all-time highs.

You could have made plenty of money by trading all three of these names, but only if you’d bought them long enough before the bubble that you’re still sitting on gains.

All the rest are down 84% or more. All but five are down 91% or more. Two have a Q at the end of their ticker symbol, indicating that they’re bankrupt. In other words, electric-vehicle stocks are a total bloodbath.

Consider the Global X Autonomous & Electric Vehicles Fund (DRIV).

The fund started trading in April 2018 at around $15 per share. It surged to about $32 in November 2021, along with the rest of the tech stocks, and today it’s around $23 per share… well above its IPO price.

The fund’s largest component isn’t one of the big electric-car makers – not Tesla or one of the big Chinese names. Nor is it a small electric-car maker… or a battery maker…

It’s Nvidia. The wildly successful chipmaker is propping up the fund… and that’s thanks to its AI-related demand much more than its autonomous-driving products.

Along with Nvidia, the fund’s 10 largest components – which make up 34.2% of its net asset value – are Alphabet, Intel, Toyota, Qualcomm, Apple, Honeywell, Microsoft, Tesla, and Hitachi. The fund also includes other automakers like Honda, General Motors, Volkswagen, Ford, Kia, Hyundai, and Nissan, among others.

Of these stocks, only Tesla is a major maker of electric vehicles.

EVs make up 12% of VW’s sales but less than 10% for Hyundai and less than 5% for every other established automaker in the fund.

Pure EV makers account for just 5.4% of the fund. Nearly half of that total is Tesla. And the fund doesn’t even touch BYD or Li Auto, the two best performers on Bilello’s list.

Now, I could see how this would be a decent way to bet on EVs but that’s only because many of these companies have so little at stake that it doesn’t matter if their EV-related business succeeds…

So, these companies might succeed and, as a group, keep generating a positive return over the fund’s IPO price.

And theoretically, you could buy DRIV in the hope that its holdings will suddenly develop big, profitable EV businesses.

But it’s much more likely that a good return would be the result of all the non-EV stuff they do – their real businesses – and not their EV bets.

After $100 billion invested in self-driving technology, autonomous vehicles are “going nowhere,” as Bloomberg declared in its headline.

I expect that autonomous-driving evangelists decried the article at the time… complaining that its closed-minded author failed to recognize the technological breakthrough that was surely just around the corner.

Instead, since the article came out, autonomous driving has gotten even further from reality. In October 2023, a self-driving electric taxi from General Motors’ Cruise subsidiary ran over a San Francisco pedestrian, dragged her 20 feet, and then parked on top of her. In response, Cruise – once America’s largest robotaxi operator – lost its license to operate in California. It ended up indefinitely mothballing its entire nationwide fleet of nearly 1,000 cars.

Meanwhile, starry-eyed analysts valued Alphabet’s Waymo self-driving subsidiary at $175 billion as recently as 2018… while an actual investment in the company valued it at a mere $30 billion (83% less) just two years later.

To their credit, the Global X folks put most of the DRIV fund into plenty of decent (and some excellent) companies that may or may not benefit from electric vehicles and autonomous-driving technology… and won’t suffer much if it fails.

A similar ETF, the iShares Self-Driving EV and Tech Fund (IDRV) started up on April 16, 2019, has about $276 million of assets, and has largely tracked DRIV’s performance. IDRV is more heavily weighted toward actual EV makers, though – so, not surprisingly, it has lagged DRIV.

That doomed proposition is available to you in the form of the Direxion Daily Electric and Autonomous Vehicles Bull 2X Shares (EVAV). It went public in August 2022 and is down about 90% since then.

Some of the once-hot EV makers are going to zero. And even the three profitable companies – Tesla, BYD, and Li Auto – remain exorbitantly valued even after their recent slumps. And the future growth they’d need to justify those valuations is nothing like a slam dunk.

Telsa’s revenue growth rate has fallen dramatically in the last two years, from 70% in 2021 to less than 19% last year. I suspect it won’t sustain even double-digit growth from here, which is what it would need to justify its current market valuation.

You get the point. This is a classic case of overpaying for overhyped growth expectations that are already starting to look long in the tooth.

US Economy

- The U. Michigan’s consumer sentiment index jumped this month, boosted by stock market gains, firmer home prices, and a robust job market.

- Households are more upbeat about their financial situation, and expecting faster gains in home prices.

- Inflation expectations declined again.

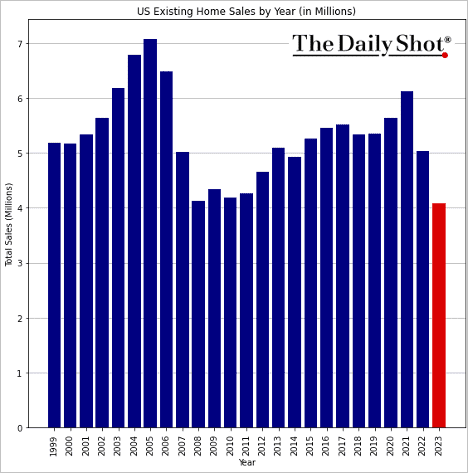

- Existing home sales held at multi-year lows in December, with the lowest annual sales in decades.

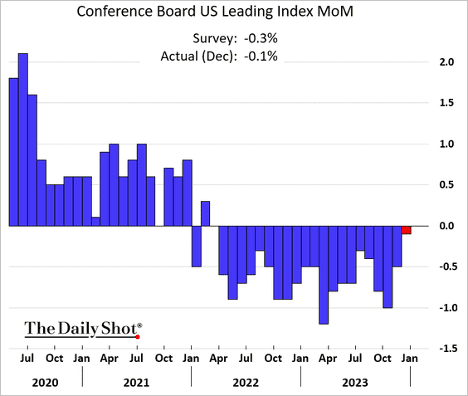

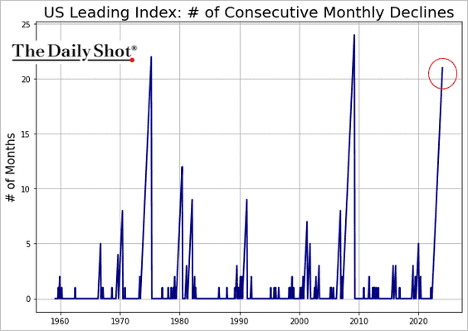

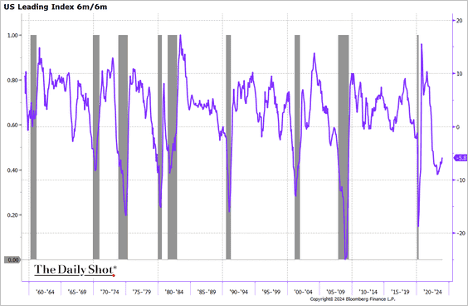

- The Conference Board’s US leading index experienced another decline last month, albeit a smaller decrease than anticipated.

- Twenty-one months of consecutive declines is unusual for this indicator.

- The index has never experienced such a large 6-month decline without a recession.

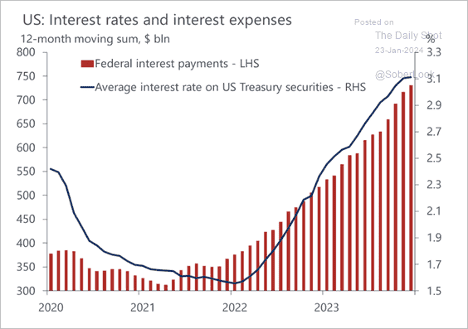

- The federal government’s interest expense is steadily rising.

Market Data

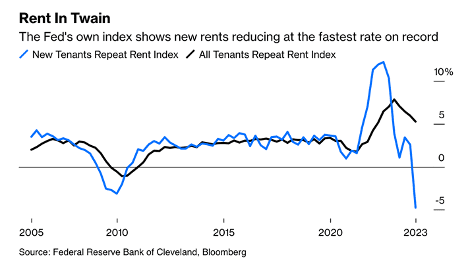

- One of the bright spots of the recent economic reports, including the CPI and PCE, is that sky-high rents have come down at a brisk pace. See rent chart below:

Great Quotes

“People who say it cannot be done should not interrupt those who are doing it.” – George Bernard Shaw

Picture of the Week

Ruins of St. Dwynwen’s Church, Ynys Llanddwyn, Wales

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}