Russia announced Wednesday it would halt natural gas flows to Poland and Bulgaria. Gavekal’s Tom Holland and Nick Andrews think this was really a warning aimed at Germany. A sudden stop in gas imports would have severe effects on the entire EU economy, and is starting to look more likely.

Key Points:

- Germany plans to reduce reliance on Russian gas, but implementation will take 2-3 years.

- The Bundesbank estimates a sudden cutoff would cause an additional 2% GDP contraction and add 1.6 percentage points to an already-high inflation rate.

- Natural gas rationing would force many industrial plants to close, since they can’t repeatedly shut down and restart.

- This could trigger high unemployment when the entire EU has little room for new fiscal and monetary stimulus.

- Pressure would rise from southern Europe for mutual EU debt issuance, which Germany has long sought to avoid.

- Given these alternatives, Germany will likely drag its feet on aiding Ukraine and meet Russia’s demand to pay for gas in rubles.

The most important decisions here are being made in Moscow, not Berlin. A Russian gas cutoff would trigger an economic downturn comparable to COVID or the 2011-2012 euro crisis. That’s a potent weapon if Putin chooses to use it.

US Economy

- The manufacturing index showed robust factory activity across the US this month.

- Export orders picked up momentum.

- Manufacturers are rapidly boosting prices.

- The services PMI measure was much less upbeat, with price pressures hitting extreme levels.

- As we saw last week, the Philly Fed’s report showed supplier delays peaking. And manufacturers expect bottlenecks to ease further in the months ahead.

- Slower demand should begin to alleviate inflationary pressures.

- And tighter financial conditions are expected to lessen demand, as the Fed’s tightening and other factors chip away at US liquidity

- Household budgets have been squeezed by inflation.

- The Dallas Fed’s manufacturing index slumped this month

- Manufacturers are very concerned about future orders

- Economic momentum is weakening. Softer demand is showing up in slower trucking activity

- While revenues are holding up for US corporates announcing earnings this quarter, profits are under pressure

- The Q1 GDP growth consensus is 1.1%.

- Home price appreciation reached 20.2% in February, a new high.

- Deteriorating affordability is denting housing demand.

- Pending home sales were softer than expected in March, declining almost 9% from the same time last year.

- The dip in mortgage applications points to further weakness in home sales.

- According to Morning Consult, discretionary spending declined last month.

- The Conference Board’s differential between consumer expectations and current conditions continues to sink. The bottoming of this spread tends to precede recessions.

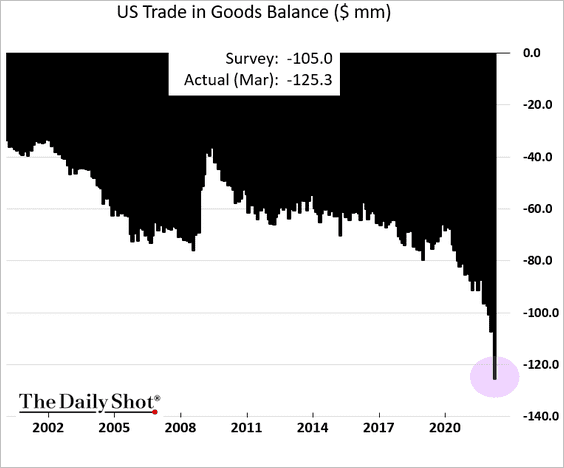

- The US trade deficit in goods hit a new record, as imports sharply outpace exports. This result doesn’t bode well for the GDP report

- The US dollar continues to surge due to the Fed’s hawkish stance relative to other central banks. This trend should help ease inflationary pressures by reducing the cost of imports and weakening commodity prices.

- Russia reported rosy March economic figures across the board. It appears that Moscow doesn’t want the West to know that the sanctions are having an impact. The Federal Service of State Statistics has lost credibility.

- The GDP unexpectedly contracted in the first quarter.

- Zooming in, we see that the main driver of the decline was the record trade deficit. Inventories and slower government spending were the other two detracting components.

- However, real final sales to domestic purchasers climbed 2.6%, suggesting that the core of the economy remains robust.

- Jobless claims are holding near multi-decade lows.

- The Kansas City Fed manufacturing index pulled back from the highs this month as demand slowed.

- Price pressures are at extreme levels but most factories are able to pass on higher costs to their customers.

The Fed

Mester is the head of the Cleveland Fed and a 2022 voting member of the FOMC, the Fed committee that decides on interest rate hikes. Loretta Mester is a 63-year-old academic economist. She joined the Philly Fed in 1985, a freshly minted Princeton PhD, and has never worked outside of the Federal Reserve system. Never.

It’s going to seem like I’m picking on Mester, but everything I say about her and every quote I have from her could just as easily be said about or quoted from any other Fed governor. They are ALL part of the same inbred, arrogant, frequently wrong but never in doubt, Soviet nomenklatura-esque priesthood of central economic planning and control.

- John Williams , head of the NY Fed, has never held a job outside of the Federal Reserve system.

- Jim Bullard , head of the St. Louis Fed, has never held a job outside of the Federal Reserve system.

- Esther George , head of the Kansas City Fed, has never held a job outside of the Federal Reserve system.

- Mary Daly , head of the San Francisco Fed, has never held a job outside of the Federal Reserve system.

- Charles Evans , head of the Chicago Fed, has never held a job outside of the Federal Reserve system and academia.

- Raphael Bostic , head of the Atlanta Fed, has never held a job outside of the Federal Reserve system and academia.

- Kenneth Montgomery , interim head of the Boston Fed since Eric Rosengren resigned in disgrace, has never held a job outside of the Federal Reserve system.

- Meredith Black , interim head of the Dallas Fed since Rob Kaplan resigned in disgrace, has never held a job outside of the Federal Reserve system.

- Patrick Harker , head of the Philadelphia Fed, is not a Fed lifer. No, he’s an academia and government lifer.

- Thomas Barkin , head of the Richmond Fed, is also not a Fed lifer. No, he’s a former senior partner and CFO at McKinsey. LOL. Oh and fun fact… while she’s no longer a regional Fed president (but is on the Fed board of governors), Lael Brainard had a stint at McKinsey as her only job outside of government and academia. So weird.

- And then there’s Neel Kashkari , head of the Minneapolis Fed. Neel is just a stalking horse.

Anyhoo… here’s part of the transcript of Mester’s interview:

Q: The White House argues the true read of the economy is the strong jobs market. Do you believe employment is so strong, too strong to actually generate a recession?

MESTER: I think we can reduce that excess demand relative to supply without pushing the economy into a recession. So, I’m pretty optimistic we can do this. It’ll be challenging, but I think we can do it. And certainly my modal forecast of what’s going to happen this year is that the expansion will continue.

“My modal forecast”

Not “model” but “modal,” as in mean, median, and mode, as in run some econometric simulations and see whatever the most frequently observed outcome looks like. It is—and I mean this in all literal seriousness—the modern equivalent of cutting open a dozen rams and examining their entrails to see what the most typical pattern looks like.

Here’s what Loretta Mester saw in her modal forecasts last year.

“I expect some higher inflation measures in the next couple of months but that is different from underlying inflation levels reaching 2%.” —Feb. 28, 2021

“I am unconcerned with inflation running away from us.” —April 5, 2021

“I’m not worried about inflation getting out of control.” —May 5, 2021

“The Fed needs inflation expectations and real inflation to rise.” —May 6, 2021

“I’d like to see inflation rise to 2% or higher.” —May 14, 2021

“By the end of the year, I expect inflation to be between 3.5% and 4%, with a drop in 2022.” —Aug. 27, 2021

“Inflation will be little more than 2% in the next years.” —Sept. 24, 2021

But wait, there’s more. It’s not just that Mester and the entirety of the Federal Reserve economic research team—more than FOUR HUNDRED PhD economists with a budget of literally hundreds of millions of dollars—got the 2021 transition to an embedded inflationary environment completely and utterly wrong, it’s also that Mester et al. got the prior embedded deflationary environment completely and utterly wrong.

What has the last decade-plus of Fed interest rate cuts and balance sheet expansion given us? Not stable prices with healthy 2% inflation expectations.

No, the last decade-plus of Fed monetary policy has given us this, the worst stretch of labor productivity growth in the history of the United States of America , not coincidentally occurring alongside the greatest stretch of financial asset appreciation in the history of the United States of America.

Market Data

- Stocks are under pressure from the Fed’s rate hike “front-loading,” as financial conditions tighten.

- The latest survey of Big Money by Barron’s shows that large money managers are extremely pessimistic about the prospect for stocks. This is not a contrary indicator, as the S&P 500’s worst returns tended to occur when these managers were pessimistic.

- The correlation between commodities and stocks is now most negative since the financial crisis.

- At -22%, the Nasdaq Composite drawdown is comparable to the last two major drawdowns in December 2018 and March 2020.

- The S&P 500 futures are at support.

- According to Truist, the S&P 500 has support at the P/E multiple of 18x. If we go through that, the next level is 17x.

- The S&P 600 (small-cap) forward P/E ratio dipped below 13x

- and the Nasdaq 100 dropped below 22x for the first time since early 2020.

- Economic data are also signaling softer earnings projections.

- Dip buyers have been getting punished, with prolonged declines not seen in decades.

Quote of the Week

There is joy in being easily amazed.

Picture of the Week

All content is the opinion of Brian J. Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}