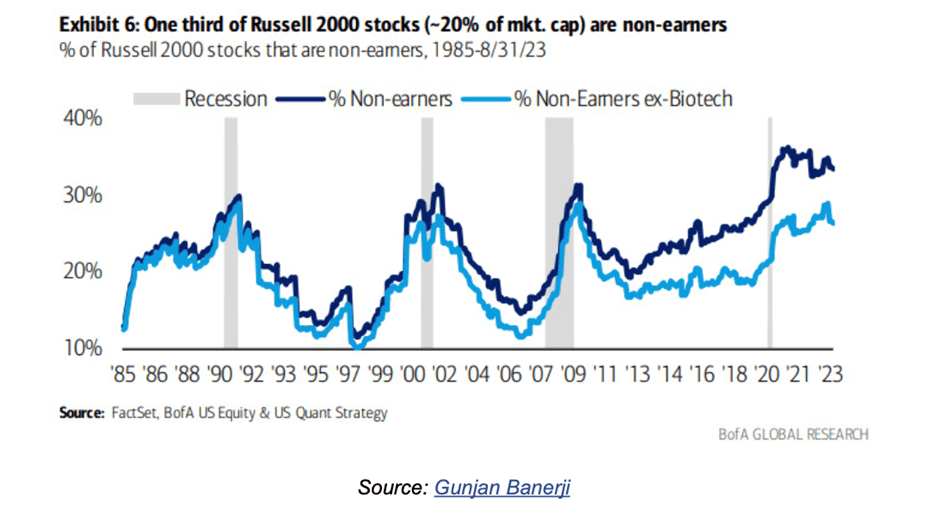

Small-cap companies are widely (and correctly) seen as riskier than larger, more established businesses. That means this chart showing that about one-third of the Russell 2000 has no earnings isn’t entirely surprising. But the percentage is considerably higher than seen in the past, even during weak economic times. Why is that?

One answer is in that word: “earnings.” Public companies have considerable bookkeeping latitude, so maybe they’re less inclined to arrange their affairs in ways that produce earnings. Cash flow, for instance, might show a different picture. But that light blue line shows another suspect. It’s the percentage of non-earners, excluding biotech companies. By that measure, today’s percentage is near where it was at the past three cycle peaks. Losses at biotech companies appear to account for much of the difference. Losses are normal in small-cap biotech, where the business usually consists of massive research spending and zero revenue. Those who actually develop a profit-generating product tend to get acquired and leave the Russell 2000. Maybe the chart shows a kind of survivorship bias. In the big picture, more biotech companies losing more money may increase the number of medical breakthroughs, helping everyone. If so, this chart is actually good news… though shareholders of the failing companies probably don’t see it that way.

Top Heavy Index

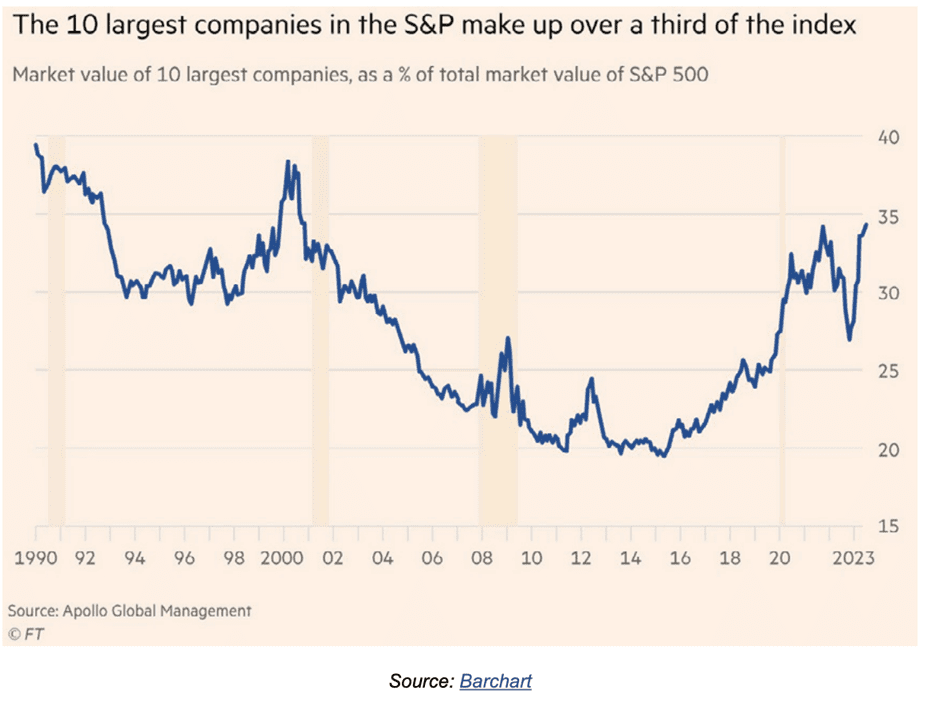

We have another anomaly on the opposite side of the capitalization scale. The combined market cap of the 10 largest S&P 500 companies presently accounts for about a third of the index value. The remaining two-thirds is split among the other 490 components.

The index was even more top-heavy around the year 2000. It was a different set of companies back then, including names like General Electric, Exxon, and Walmart, along with the tech giants. Today’s top tier is pure technology. Something else notable in the chart: The top 10’s percentage fell steadily from 2000 until around 2015 when it began an extended recovery. Why was that? What changed?

The Fed

The FOMC minutes showed the Fed’s ongoing concerns about upside risks to inflation.

These risks included the imbalance of aggregate demand and supply persisting longer than expected, as well as risks emanating from global oil markets, the potential for upside shocks to food prices, the effects of a strong housing market on shelter inflation, and the potential for more limited declines in goods prices.

… amid robust economic growth.

Some participants remarked that an upside risk to their projections for economic activity was that the unexpected resilience that the economy had demonstrated so far could persist.

The focus has shifted from the level of the terminal rate to “higher for longer” .

All participants agreed that policy should remain restrictive for some time until the Committee is confident that inflation is moving down sustainably toward its objective.

… to reduce the risk of “reacceleration.”

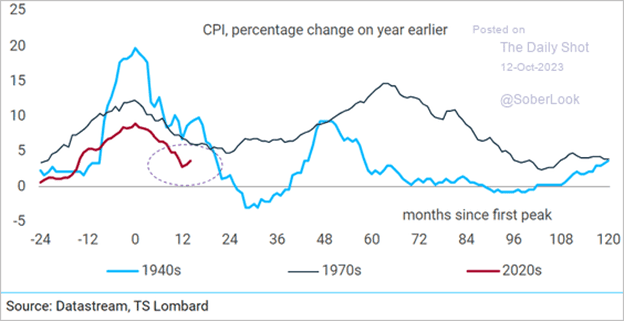

Source: TS Lombard

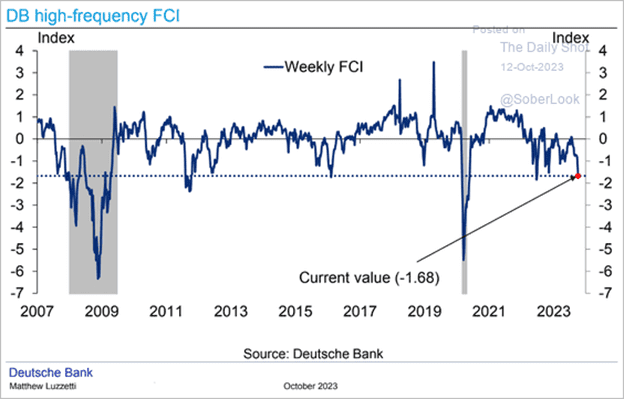

But with Treasury yields surging since the FOMC meeting and financial conditions tightening sharply (chart below), the minutes represent stale information

Source: Deutsche Bank Research

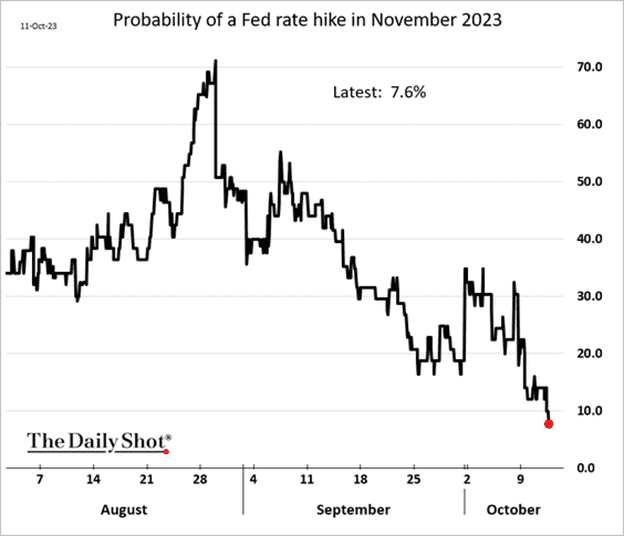

At this point, the market does not expect a rate hike in November.

US Economy

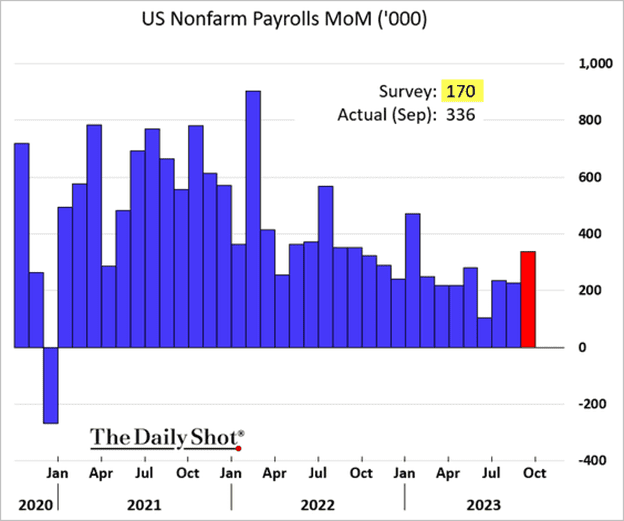

The September jobs growth figure was almost double the expectations.

- Gains were broad, with hotels and restaurants, logistics, retail, healthcare, business services, and government (mostly educators) all registering payroll increases.

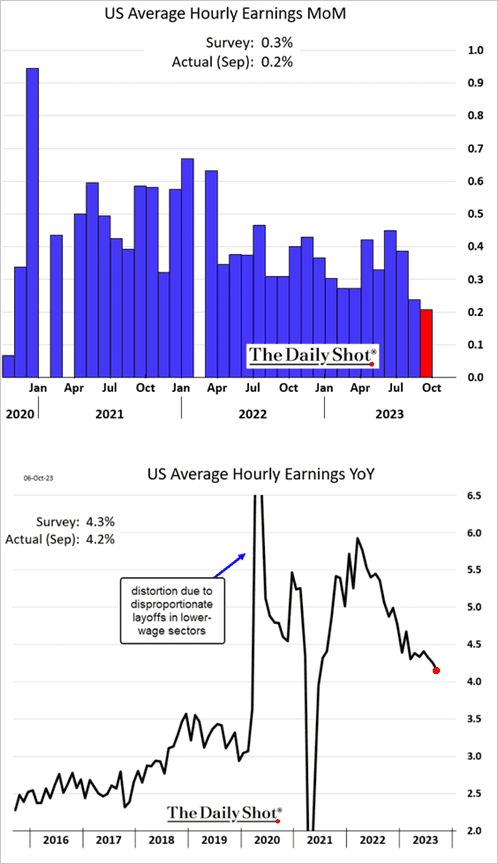

- Wage growth surprised to the downside.

- The unemployment rate held steady, and underemployment edged lower.

- The declines in temp services continued but at a slower pace.

- Labor force participation held steady.

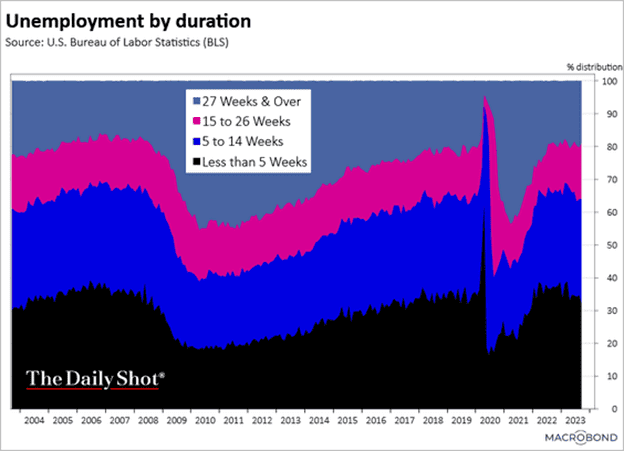

- Here is a look at unemployment by duration.

- Banks (lenders continue to reduce staff)

- Construction (resilient)

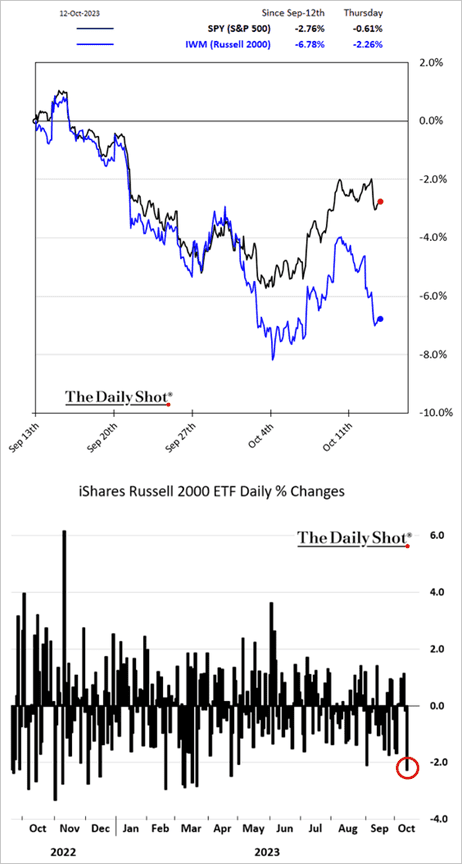

- Risk assets sold off initially but then took solace in slowing wage growth. However, all bets are off with escalating violence in the Middle East.

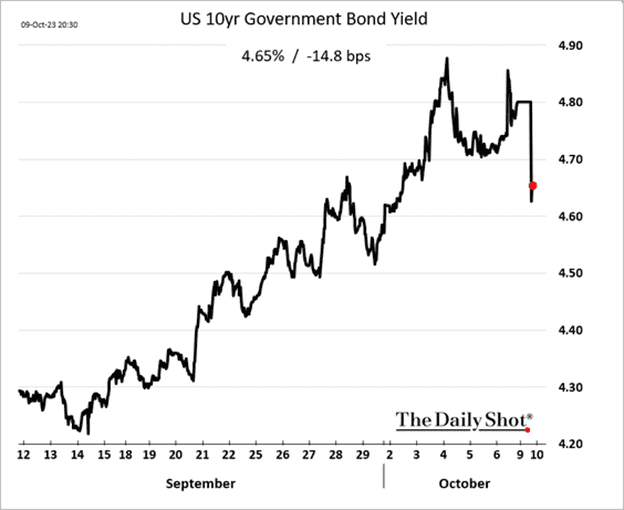

- 10-Year Treasury yields managed to hit new 1-year highs at 4.8%, and the yield curve steepened further.

- The market still sees about a 50% chance of another Fed rate hike.

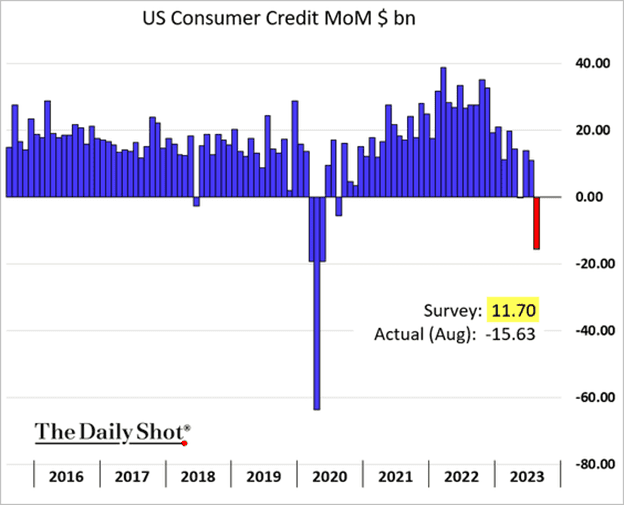

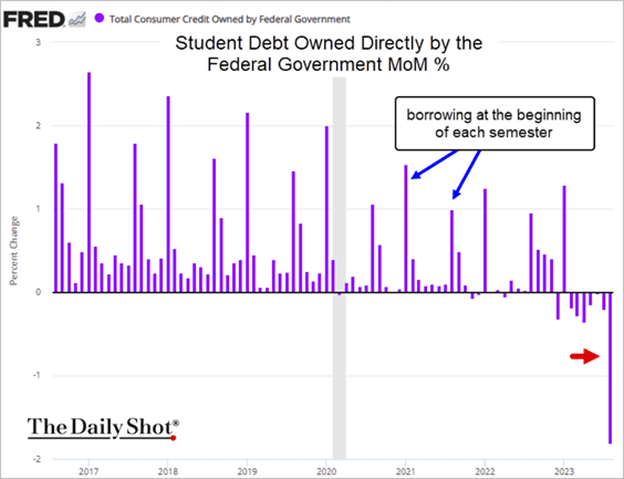

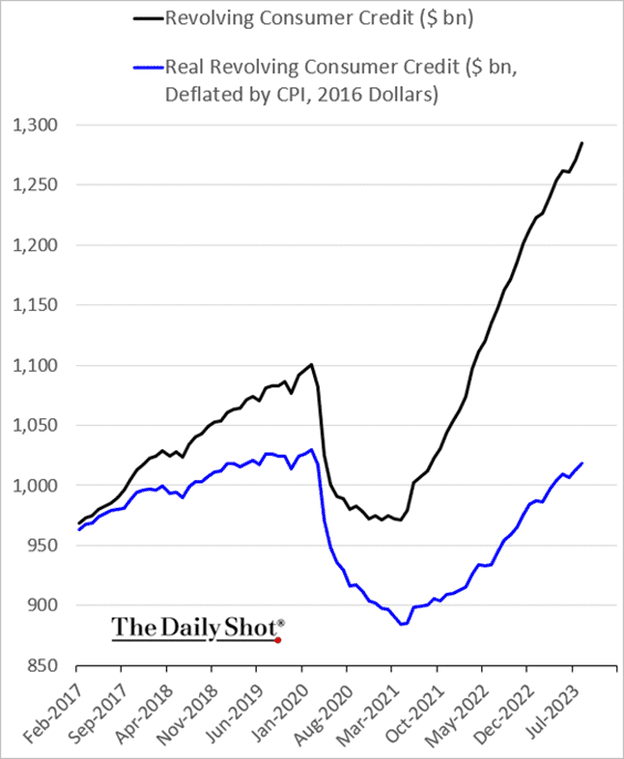

- Consumer credit tumbled in August, …

- … as borrowers paid down some of their student debt.

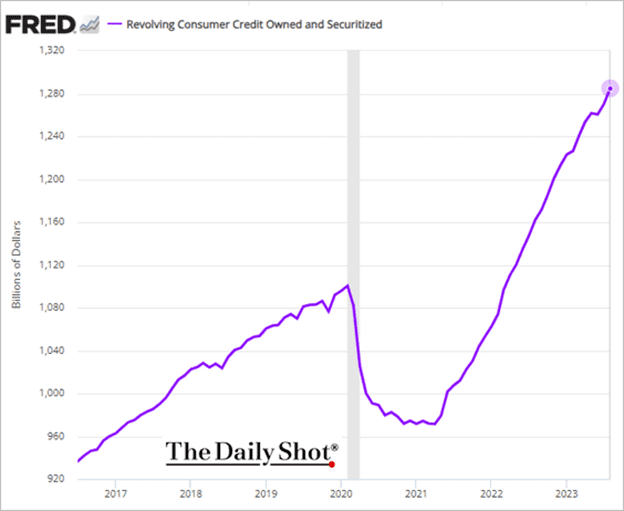

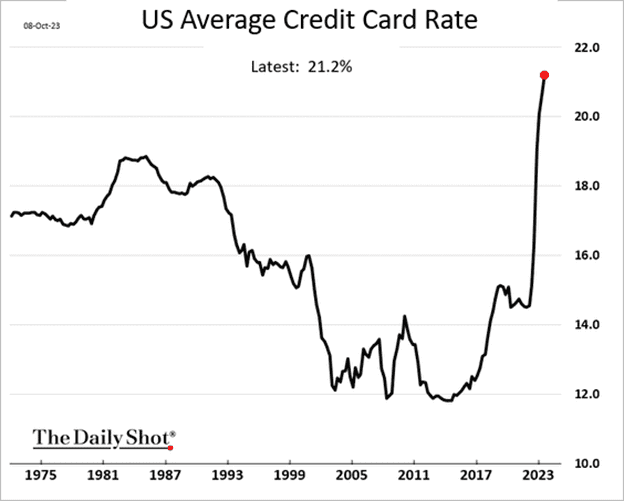

- Credit card balances continued to climb, …

- despite record rates.

- Inflation-adjusted credit card loan balances:

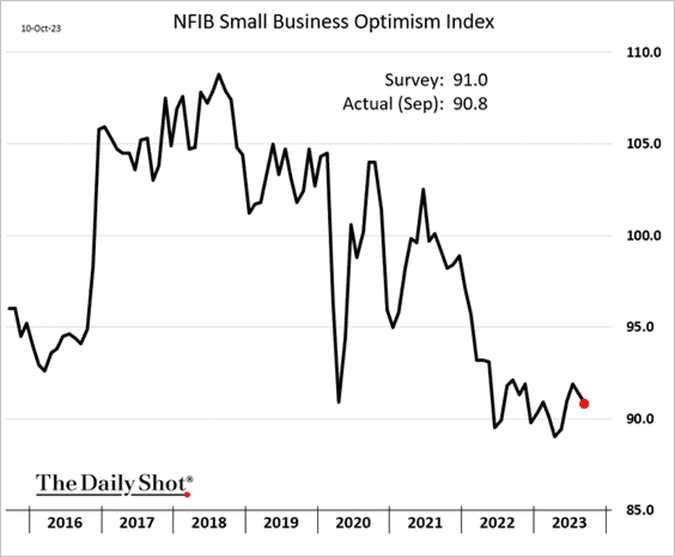

- The NFIB small business sentiment indicator declined last month.

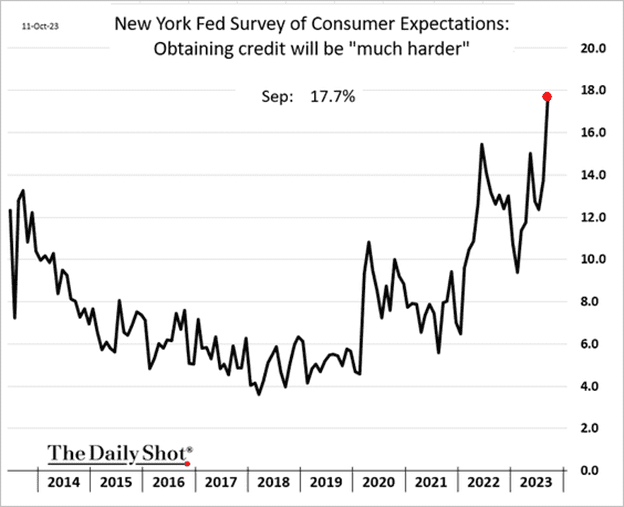

- The share of US consumers who anticipate significant challenges in securing credit is on the rise.

- Inflation expectations rose last month, as reported by the NY Fed’s Survey of Consumer Expectations, likely due to the increase in gasoline prices.

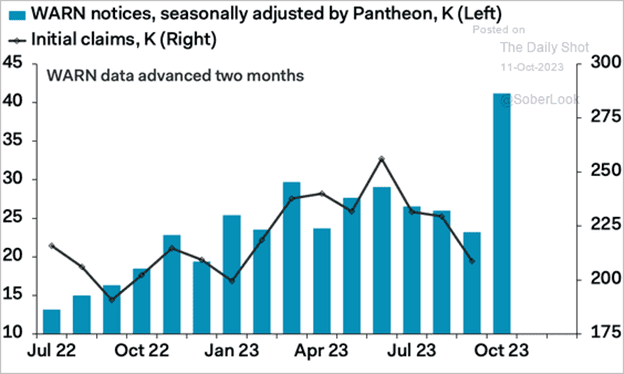

- WARN notices suggest that jobless claims will jump this month. Under the WARN Act, companies with over 100 employees must provide a 60-day notice ahead of any planned closures or mass layoffs.

- The number of workers on strike hit a multi-year high.

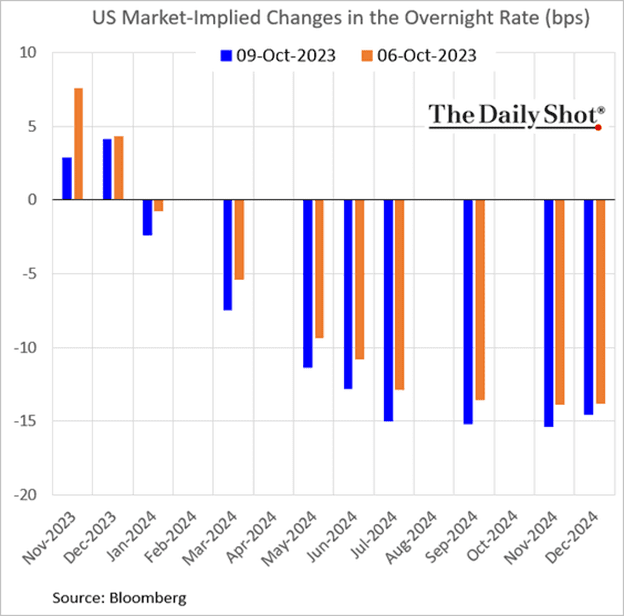

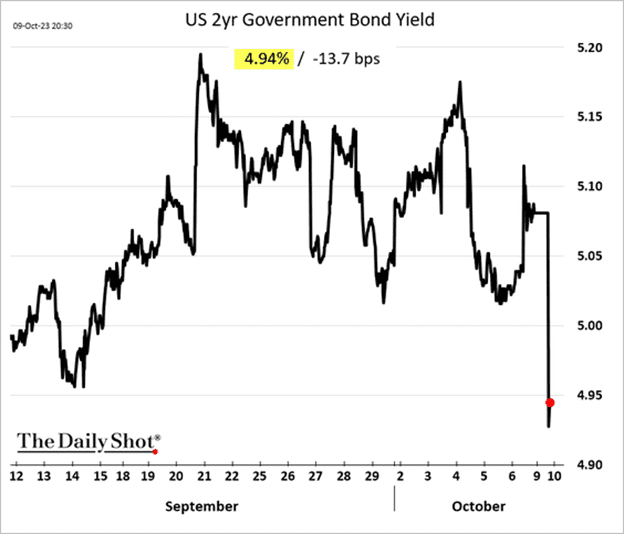

- Fed officials are growing concerned about the surge in Treasury yields, with financial conditions tightening substantially in recent weeks. If there were intentions to raise rates further, the market has effectively taken that initiative.

Source: Reuters Read full article

Source: Reuters Read full article

- The probability of a rate hike in November declined, …

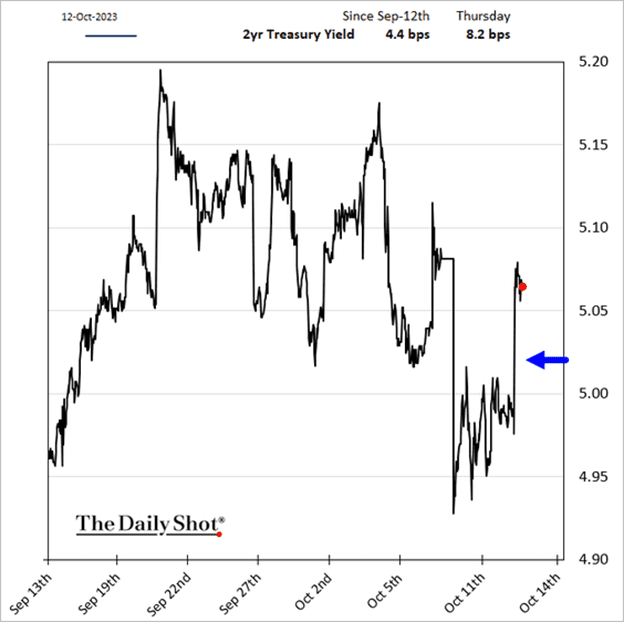

- Treasury yields dropped sharply, …

- … with the 2-year rate dipping below 5%.

- It was the best day for Treasuries in months.

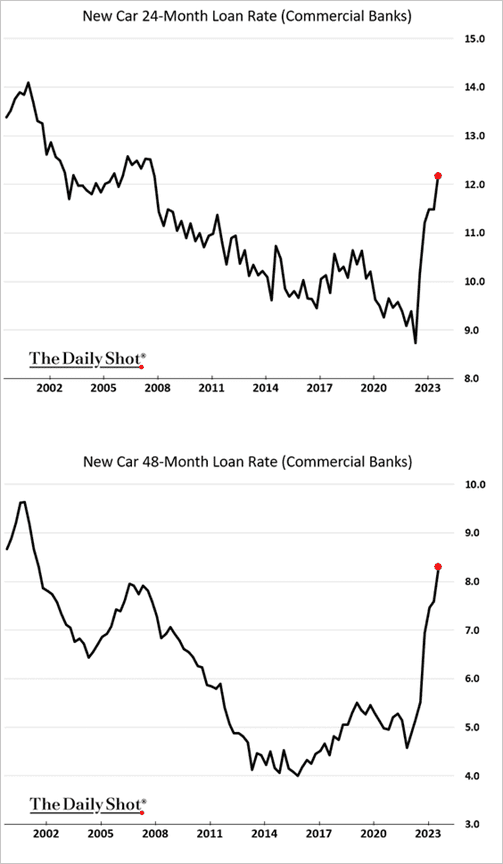

- US commercial bank auto loan rates are at the highest levels since 2008.

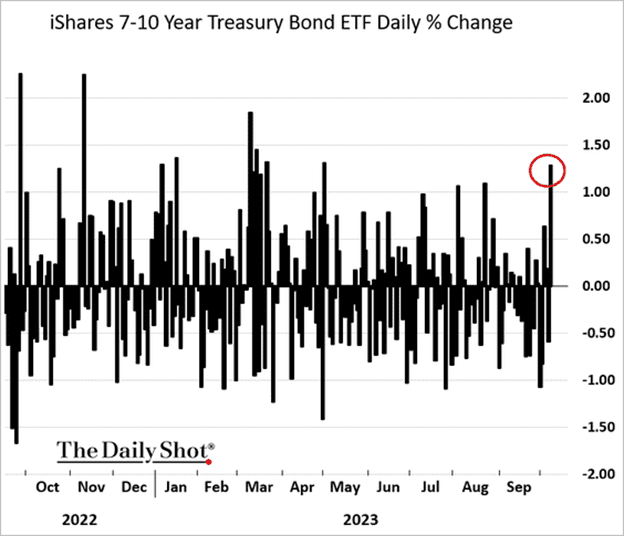

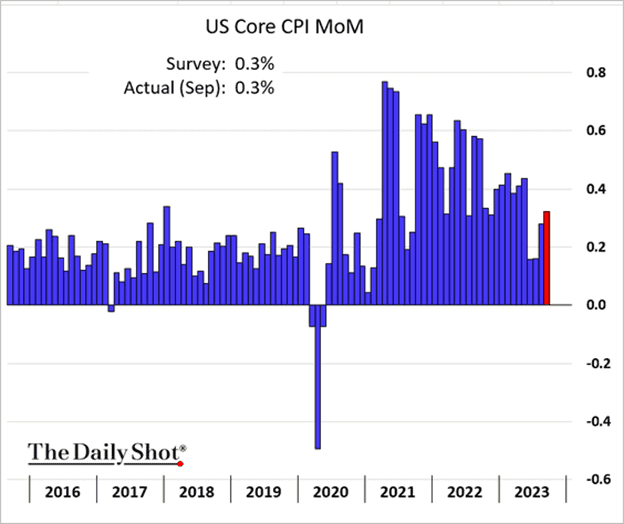

- The September CPI report topped expectations, suggesting that the Fed’s effort to curb inflation remains a work in progress.

- Core inflation strengthened.

- The probability of a Fed rate hike in December increased in response to the CPI report. November still seems to be off the table.

- Treasury yields surged, with the 2-year rate climbing above 5% again.

- The dollar jumped.

- Risk assets retreated.

- Commodities went down

- US jobless claims are holding just above multi-year lows for this time of the year.

- But continuing claims remain elevated.

- US housing inventories remain tight.

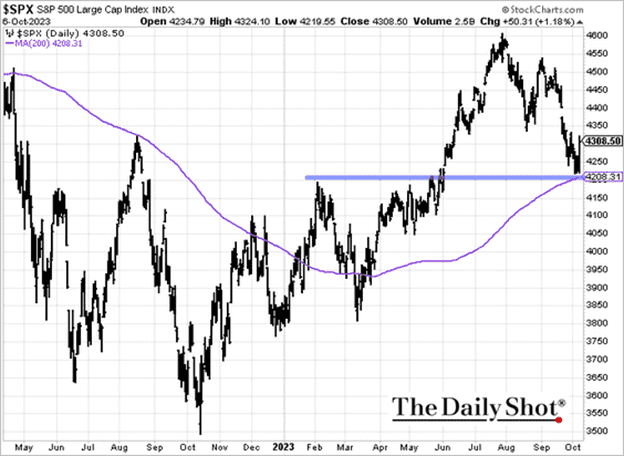

Market Data

- The S&P 500 held support as US wage growth slowed.

- The S&P 500 concentration is at the highest level since the dot-com bubble.

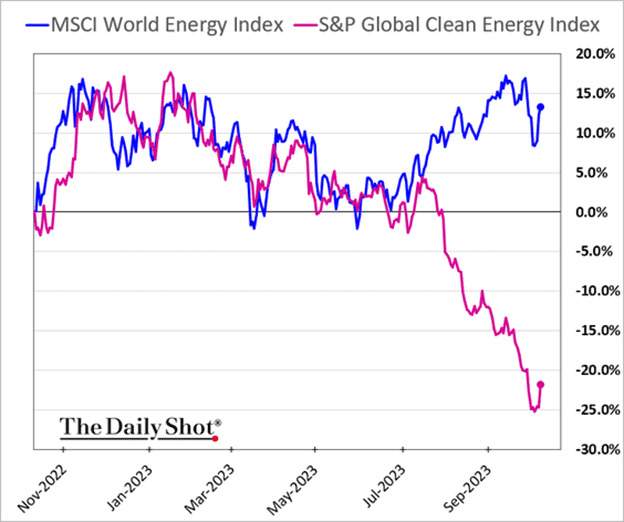

- The gap between clean energy shares and traditional energy firms has blown out.

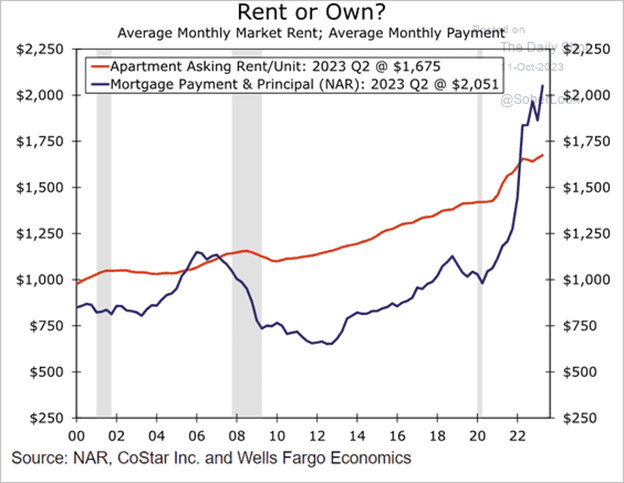

- US rental costs vs. mortgage payments:

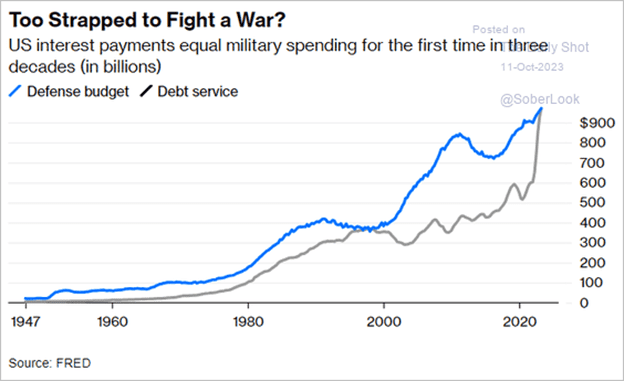

- US defense budget and debt service costs:

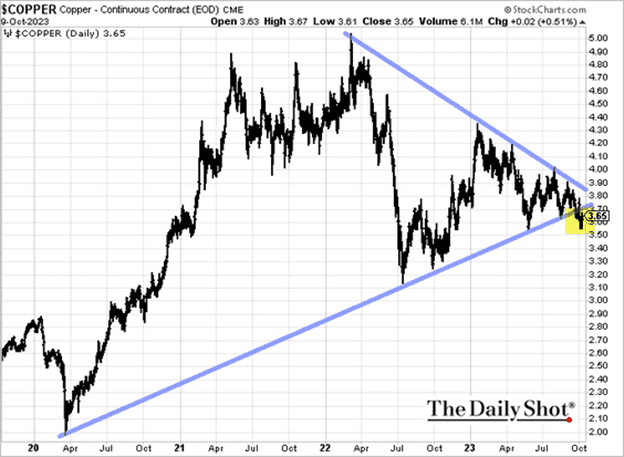

- A fakout?

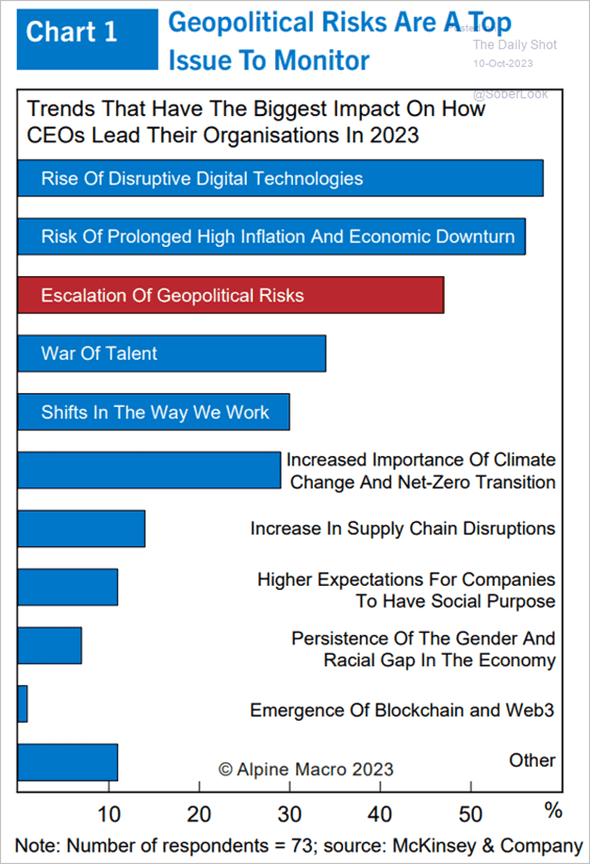

- How concerned are CEOs about geopolitical risks?

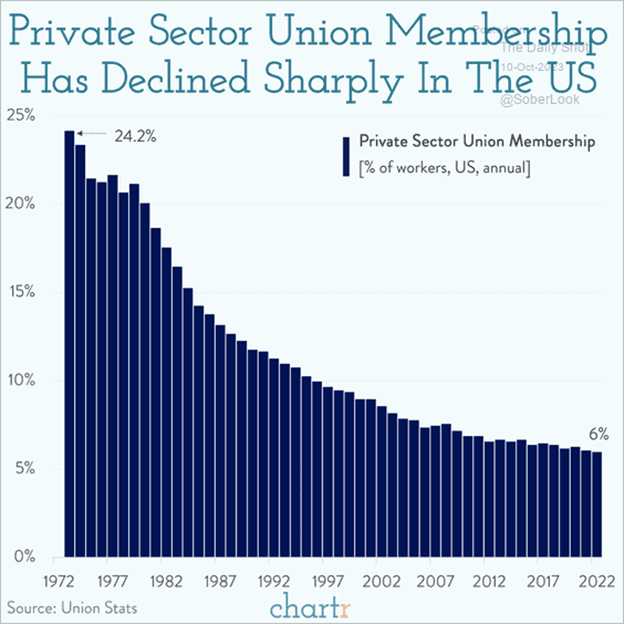

- Private sector union membership:

- Office return rates in major US cities have plateaued at around 50%

- The hotter-than-expected CPI report and a rebound in bond yields spelled trouble for small caps.

- Housing stocks also took a hit.

- Semiconductor shares have been outperforming.

Great Quotes

Mark Twain wrote to William Vanderbilt’s grandfather, Cornelius Vanderbilt:

“How I pity you, and this is honest. You are an old man, and ought to have some rest, and yet you have to struggle, and deny yourself, and rob yourself restful sleep and peace of mind, because you need money so badly. I always feel for a man who is so poverty ridden as you.

Don’t misunderstand me, Vanderbilt, I know you have $70 million. But then you know and I know, that it isn’t what a man has that constitutes wealth. No – it is to be satisfied with what one has; that is wealth.”

Picture of the Week

Apulia, Italy

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}