- The November Beige Book report from the Federal Reserve.

- Economic activity was softer, with mixed regional reports. The overall economic outlook has become less optimistic.

- Labor demand eased, with most districts reporting flat to modest employment gains. The job market saw improved applicant availability and better retention rates. Despite some instances of layoffs and a greater willingness to release underperforming staff, the labor market overall remained tight, especially for skilled labor.

- Most districts reported easing wage pressures.

- Price increases subsided across districts but remained elevated.

- Consumers displayed greater price sensitivity, notably in their spending on discretionary and durable goods. This shift points to a cautious consumer environment shaped by broader economic factors.

- Key economic concerns raised include geopolitical instability, the impact of high interest rates, and looming risks of a recession.

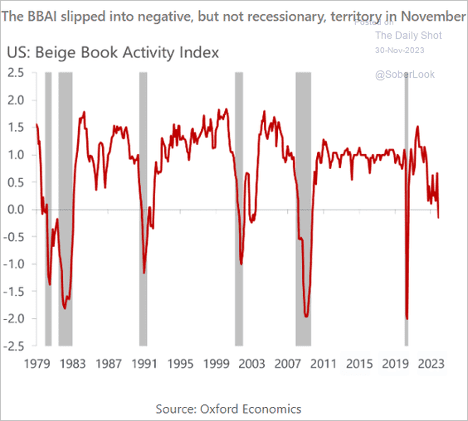

- The Oxford Economics Beige Book Activity Index dipped into negative territory for the first time since the COVID shock.

Source: Oxford Economics

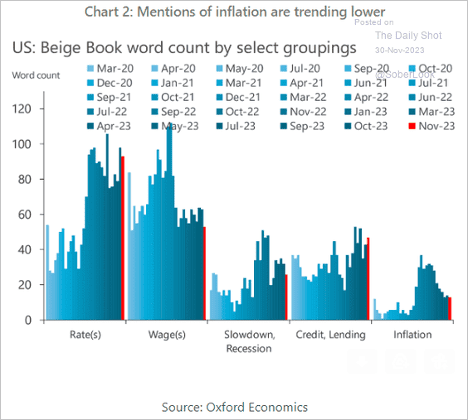

- Inflation concerns continue to moderate.

Source: Oxford Economics

Source: MarketWatch Read full article

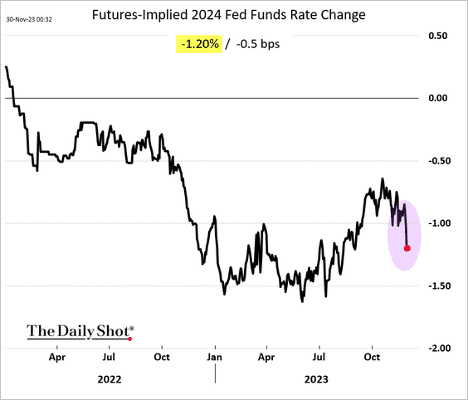

- The market is now pricing in 120 bps of Fed rate cuts next year.

The Fed

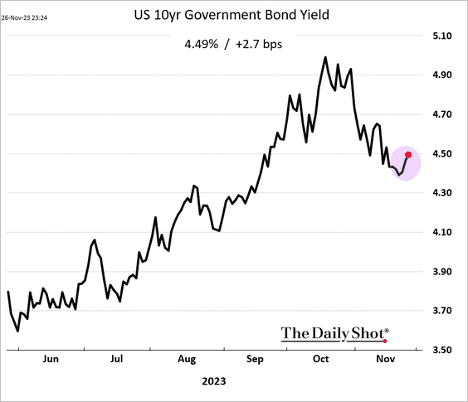

Dovish signals from the Federal Reserve are reinforcing what traders have been pricing in since the end of October, when the central bank held rates for the second consecutive meeting and a dot plot – that suggested one more hike – was called into question. Since then, stocks have risen at a rapid clip, with the S&P 500 (SP500) climbing out of correction territory in only 16 trading sessions, marking its fastest comeback since the 1970s. Besides lifting markets and risk assets, the prospect of cheaper money saw the 10-year Treasury yield drop overnight to below 4.30%, after touching 5.00% just prior to the last Fed meeting.

Two of the most hawkish FOMC officials, who led the charge for higher rates last year, are getting comfortable with holding policy steady, backing expectations that the central bank’s hiking cycle is done. Fed Governor Christopher Waller said Tuesday that he’s “increasingly confident” that monetary policy is now in the right spot to slow the economy and bring inflation back down to the 2% target. Governor Michelle Bowman also stopped short of endorsing an increase next month, conditioning the need for further hikes only on incoming data that “indicate progress on inflation has stalled or is insufficient to bring inflation down to 2% in a timely way.”

Investors appear to be even more enthusiastic, especially armed with the economic data to support them, including recent soft numbers on inflation and the job market. Odds that the central bank will even cut its target policy rate in the middle of 2024 have been on the rise, and some, like Pershing Square’s (OTCPK:PSHZF) Bill Ackman, are now even pricing in rate cuts as soon as the first quarter. As the conversation shifts from hikes to cuts, the U.S. dollar is on track to hit its lowest level in months, reflecting the revised rate expectations.

Currency considerations: “Fed-driven dollar weakness will be a story for 2024,” writes ING Economic and Financial Analysis. “The most likely path to a weaker dollar will probably have to come from softer U.S. macro data. Given our house view that a US slowdown is more likely in the next quarter rather than this one, we therefore expect EUR/USD to end the year around this 1.05/1.06 area and USD/JPY to end the year not far from 150. Into 2024, however, we expect the short end of the U.S. curve to start moving lower ahead of Fed easing next summer and the dollar to turn lower.”

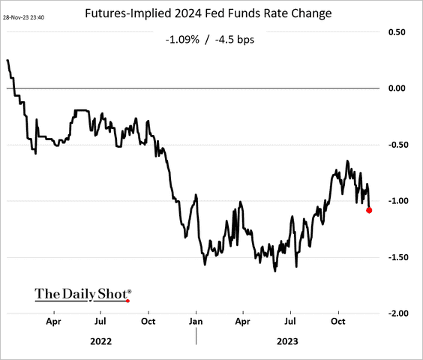

Markets are pricing in more substantial Fed rate cuts for 2024.

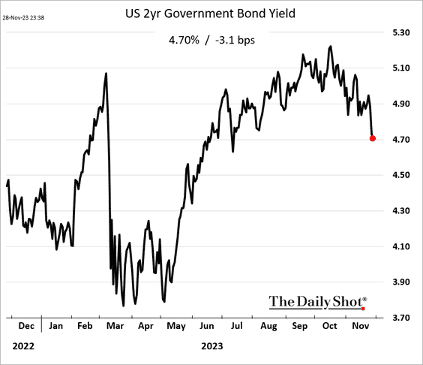

Treasury yields are down sharply this month.

US Economy

- The S&P Global flash PMI report indicated a modest expansion in the US services sector this month.

- Manufacturing activity dipped back into contraction territory.

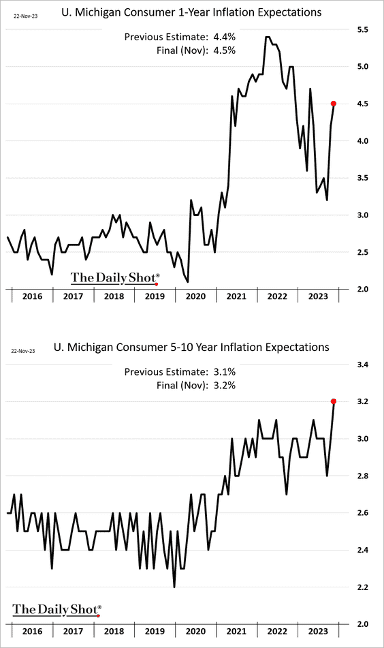

- The revised inflation expectations data from the University of Michigan highlight consumers’ concerns about inflation resurgence.

Source: Reuters Read full article

- Treasury yields moved higher in response to the University of Michigan report.

- Durable goods orders declined sharply last month, driven by the transportation sector.

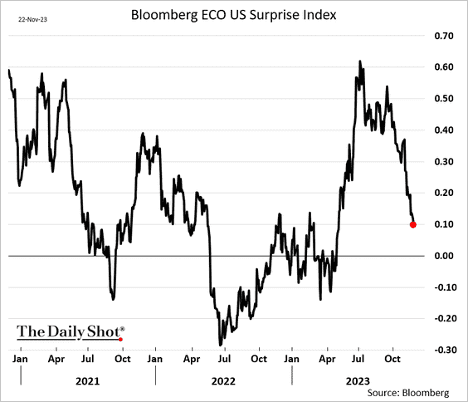

- Bloomberg’s index of US economic surprises has experienced a sharp decline in recent weeks.

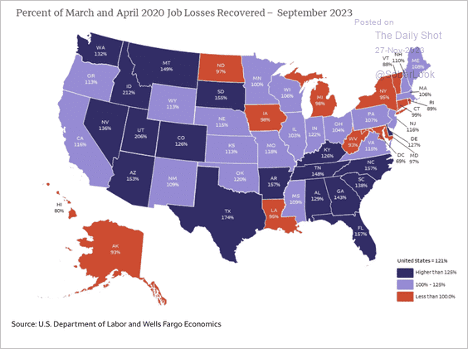

- Here is a look at the proportion of job losses each state has recovered since the onset of the pandemic.

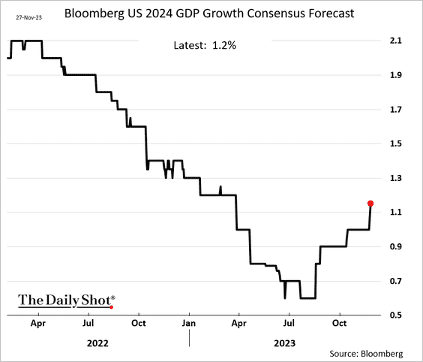

- Economists upgraded their forecasts for next year’s GDP growth, with no recession expected over the next few quarters.

- New home sales softened last month but held well above 2022 levels.

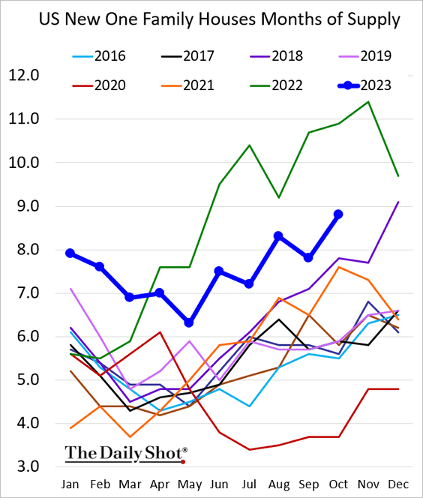

- Next, we have new home inventories in months of supply.

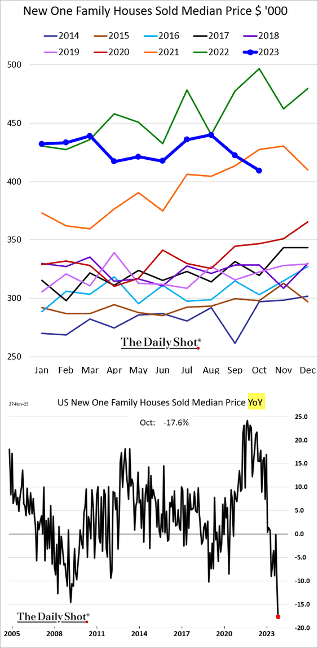

- The median new home price dropped sharply, …

- The Dallas Fed’s manufacturing report showed deteriorating Texas factory activity this month.

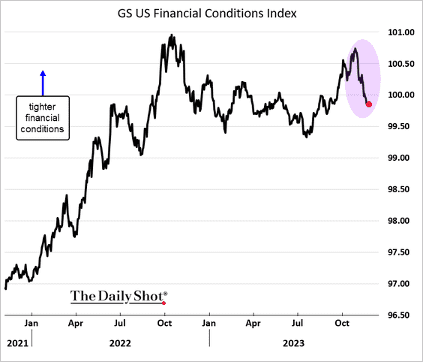

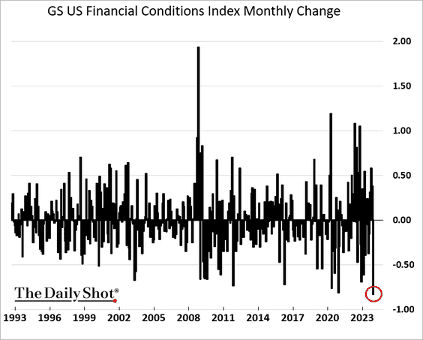

- US financial conditions eased sharply this month, …

- …..with the largest monthly decline in Goldman’s indicator in recent decades.

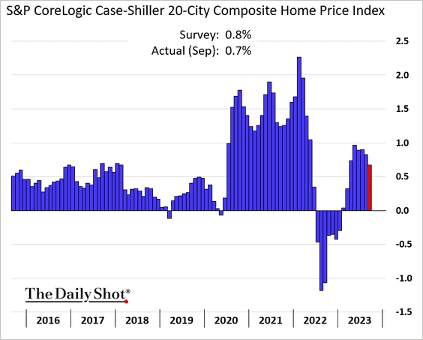

- Home prices climbed again in September, and are now up almost 4% relative to 2022.

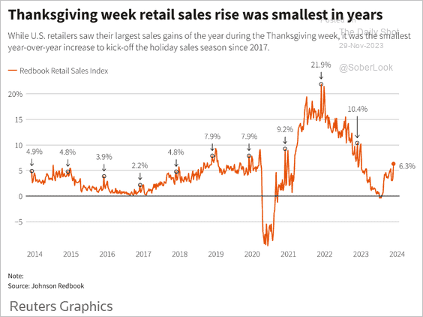

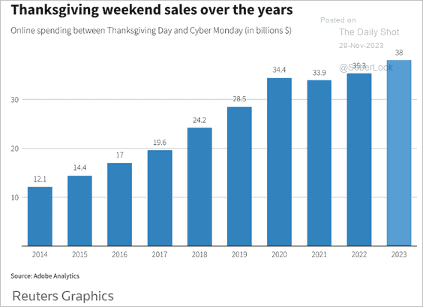

- The increase in same-store sales during the 2023 Thanksgiving week was less robust than the year-over-year gains observed in recent years.

Source: Reuters Read full article

- Online sales were relatively strong.

- Over 200 million shoppers tapped into promotions offered by retailers.

Market Data

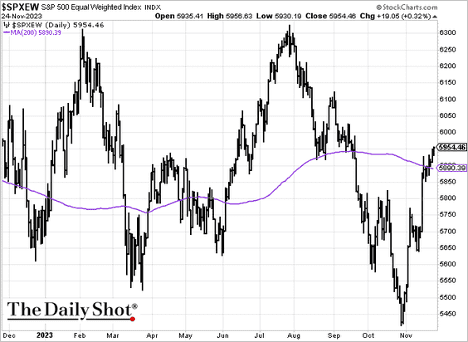

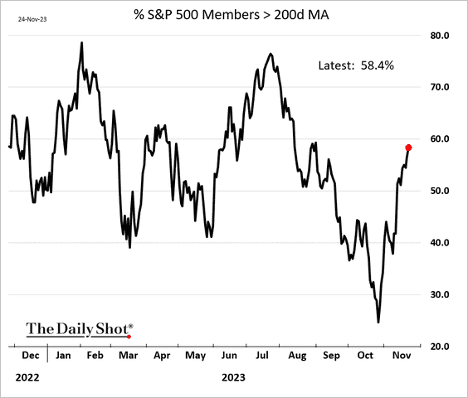

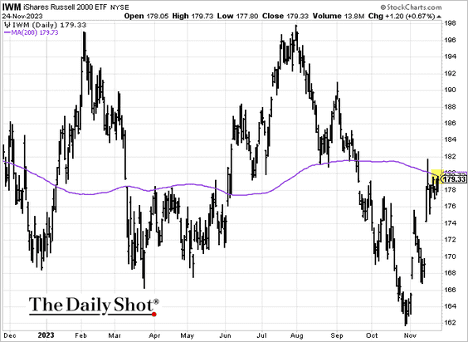

- The rally has been broadening out.

- The S&P 500 equal-weight index (above its 200-day moving average):

- The percentage of S&P 500 stocks above their 200-day moving average:

- The Russell 2000 index is holding resistance at the 200-day moving average.

- The dollar’s share of global private transactions has been rising.

![]()

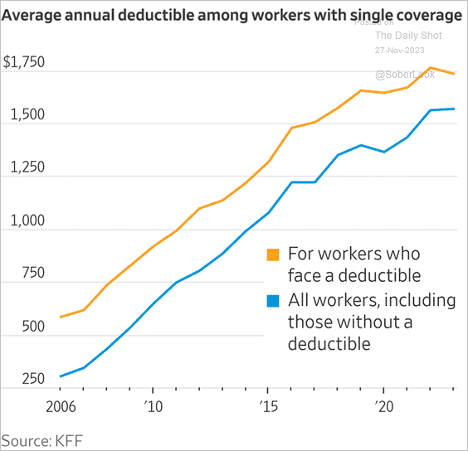

- Health insurance deductibles:

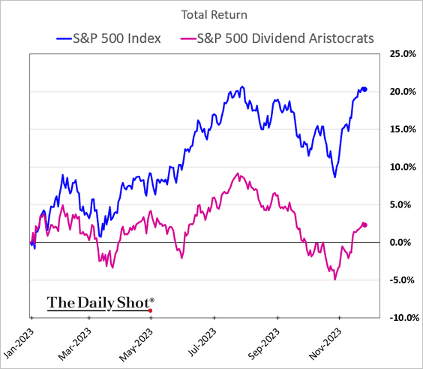

- Shares of dividend growers continue to underperform.

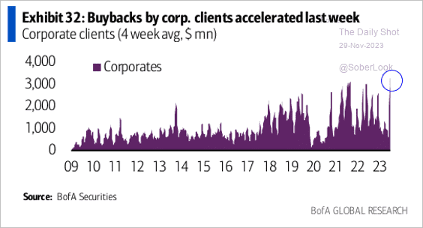

- Share buyback activity has picked up momentum.

Source: BofA Global Research; @MikeZaccardi

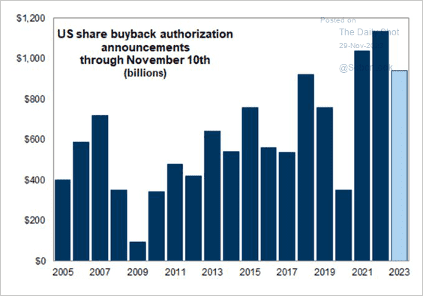

- But this year’s buybacks still lag 2022.

Source: Goldman Sachs; @WallStJesus

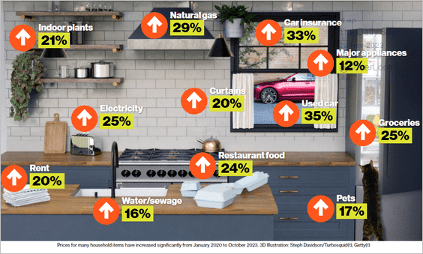

- Pandemic-era US price changes (January 2020 – October 2023):

Source: Bloomberg Read full article

Great Quotes

“Those who keep learning will keep rising in life.” – Charlie Munger

Picture of the Week

Beaches of Thailand

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}