Many of the recent sanctions leveled on Russia have power because they’re based on the U.S. dollar, which is the most widely used currency in global financial markets, trade and central bank reserves. However, some are cautioning that weaponizing the greenback in this fashion could erode its dominance, stoking fears that smaller currencies like the renminbi could gain a bigger role on the international stage. China is already buying Russian energy with the yuan, while India is looking into a rupee-ruble trade arrangement. “Wars upend the dominance of currencies and serve as a doula to the birth of new monetary systems,” cautioned Zoltan Pozsar, analyst at Credit Suisse.

This time around, the U.S. went ahead with unprecedented sanctions on Russia’s central bank, which has roughly a fifth of its $630B of foreign reserves in dollar-denominated assets. Many central banks across the globe have dollars in their “rainy day funds” given their longtime markings of continuous stability, but data from the IMF shows that reserves have been coming out of the dollar and trickling into other currencies. There was $12T worth of foreign reserves held by central banks around the world at the end of 2021, with the dollar accounting for about 59% of the total, down from 71% in 1999 (the year the euro was launched).

“This is the beginning of the end of the dollar’s monopoly in the world,” declared Vyacheslav Volodin, speaker of the Russian Duma lower house of parliament. “Anyone who keeps money in dollars today can no longer be sure that the U.S. will not steal their money.” While the ruble this week recovered all of the losses seen since the invasion of Ukraine in February, many caution that the rebound was due to severe capital controls imposed by the Kremlin, a doubling of interest rates and foreign traders being barred from exiting their investments. “Sanctions cause the U.S. to lose its credibility and undermine the dollar’s hegemony in the long run,” added Zhang Yanling, former executive vice president of Bank of China.

While the decline of the dollar has been predicted many times before, the U.S. has been through many turbulent periods with its currency still reigning supreme in global markets. America is also coordinating its sanctions with major allies, meaning other key currencies that can be used as an alternative (like the pound, euro, yen) are also off the table. Moreover, countries may be hesitant to diversify their reserves to currencies like China’s yuan, which is still not fully convertible and mixed into added geopolitical risks associated with the country. On the other hand, the U.S. market offers a level of liquidity that is not seen anywhere else in the world, backed by free markets and strong financial institutions.

US Economy

- March job gains were a bit below consensus but still substantial.

- Total employment is approaching pre-pandemic levels.

- Labor force participation continues to improve, especially for prime-age workers. This is a green light for the Fed to rapidly push up rates.

- On the whole, the labor market looks stronger than it was before the pandemic.

- After the employment report, the market priced in a high probability of nine additional 25 bps rate hikes this year.

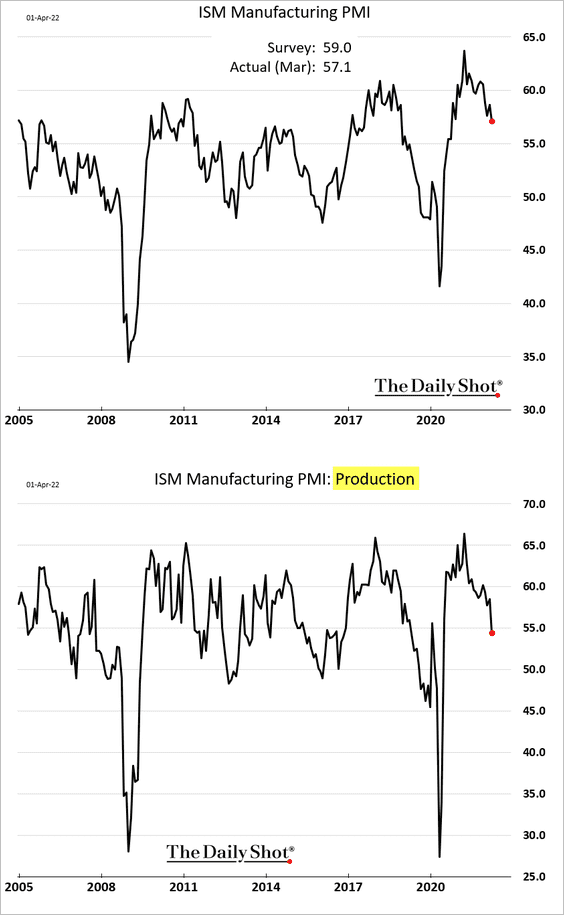

- Growth in new orders, ISM, slowed sharply, pointing to weakness ahead for US manufacturing.

- Prices pressures remain elevated.

- US vehicle sales declined again last month.

- Housing demand remains strong despite the recent spike in mortgage rates to 5%.

- More than half of US homes are sold above the list price.

- But second homes saw a pullback in demand.

- Current prices are pressuring affordability

- Demand for apartments has been surging.

- Rents have been rising quickly, but renting is increasingly cheaper than buying.

- The price-to-rent ratio does not bode well for home price appreciation going forward.

- The core PCE inflation (the Fed’s preferred measure):

- The commodity price shock (% of consumer spending):

- Retired workers are returning to the labor force, pulled by inflation and higher wages.

- The jobs/workers gap shows unusual tightness in the labor market.

- US factory orders have been very strong.

- China’s slowdown will pull global economic activity lower.

- Faced with rapid price increases, households are tapping their credit cards again.

- Jobless claims remain near multi-year lows.

- Housing market sentiment has deteriorated to multi-year lows, according to Fannie Mae.

The Fed

Fed Governor Lael Brainard said the central bank could start the balance sheet roll-off as soon as May and move at “a rapid pace.” She also seems to be on board with 50 bps rate hikes.

Since the markets view Brainard as a dove, these comments were particularly impactful. The goal here is to tighten financial conditions quickly, as the Fed plays catch-up on the inflation front. Treasury yields surged.

News of faster quantitative tightening hit longer-dated bonds hard. It was certainly one way to pry the yield curve out of inversion.

Bill Dudley said yesterday in a Bloomberg opinion piece that the Fed will have to “inflict more losses on stock and bond investors” to get inflation under control.

Dudley said…

“Equity prices influence how wealthy they feel, and how willing they are to spend rather than save.”

Members of the Federal Open Market Committee (“FOMC”) are also playing hawkish notes with dramatic flair. For example, Fed Governor Lael Brainard said Tuesday in a speech for a Minneapolis Fed discussion that the Fed will reduce its balance sheet “at a rapid pace” as early as its May 3 to 4 meeting.

She also said…

“I expect the balance sheet to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017–19.”

Shrinking the balance sheet rapidly means the Fed will actively sell U.S. Treasury securities and mortgage-backed securities… “Caps” means the limit to the amount of securities the Fed will sell. “Larger caps” means more aggressive selling.

The period Brainard cited includes the four months of September through December 2018, when the S&P 500 Index plunged 20%, as the Fed continued to shrink its balance sheet and raise interest rates.

As a former Goldman Sachs executive, Dudley will carry the mark of a vampire squid of Wall Street for eternity.

So we must ask, if Brainard’s prescription is followed and the Fed sells securities more aggressively than it did from 2017 to 2019, will a repeat of the late-2018 episode satisfy Bill Dudley’s vampire-squid blood lust for investor losses? Or will we need an extended bear market to replenish his life force?

And Brainard isn’t the only current Fed official with a flair for making hawkish comments. St. Louis Fed President James Bullard said in a speech in February that he became “dramatically” more hawkish as inflation hit 40-year highs.

Bullard also said he wanted to see “100 basis points in the bag by July 1″… meaning a one-percentage-point increase to the fed-funds rate. Bullard was the only dissenter on last month’s 0.25% interest-rate hike.

It’s worth noting that many of the other, apparently more media shy, FOMC members favored a 0.5% hike but voted for the 0.25% hike because the Ukraine war created too much uncertainty. I guess these folks value a consensus more than expressing their true opinions.

The Fed isn’t raising interest rates very fast, and cheap credit is a primary feature of most massive financial bubbles. Rates are still near all-time lows in all of recorded history. So, it’s not crazy to expect that even modestly raising rates will let some more speculative steam out of stock prices.

It’s anybody’s guess if higher rates push stocks down 20%-ish like in 2018, or a lot more, like how Bill Dudley dreams each day.

It’s also anybody’s guess what happens when the world’s biggest holder of Treasury securities and mortgage-backed securities starts selling $95 billion worth of them each month, as the Fed suggested it would do in the latest Fed meeting minutes, released yesterday.

Maybe there’ll be plenty of new demand for all the new supply. Maybe not. But we will definitely find out.

No matter what the future brings, the bond market didn’t like Bullard’s comments back in February and the stock market didn’t like Dudley and Brainard’s recent comments. When Bullard spoke, the fed-funds futures markets instantly tacked on 100 basis points, which is a gigantic move.

When Brainard and Dudley’s comments hit the tape last Tuesday and Wednesday, the big stock indexes fell. As of yesterday’s close, the S&P 500 and Nasdaq are down 6.5% and 12%, respectively, since January 1.

So, the Fed talking heads haven’t put much of a dent in the bubble. We’ll see if Dudley gets his way. For now, downside potential remains significant in a stock market.

There are basically three possible outcomes.

- The Fed tightens just enough to squelch inflation and maintain GDP growth.

- The Fed doesn’t do enough and inflation gets worse, or doesn’t come down as fast as the market or anyone else would like.

- The Fed (eventually?) does too much and we swing from high inflation to recession. Remember, recessions are by definition deflationary. They are accompanied by demand destruction.

We can hope for #1, but it’s a (very) long shot.

I think #2 is most likely.

The market is currently pricing in a 75% chance of nine rate hikes that would bring Fed Funds to somewhere between 2.5% and 2.75% by the end of the year!

Starting with Greenspan clearly boosting the housing market in the early part of the century, Bernanke/Yellen’s QE, compounded by Powell expanding QE and keeping 0% rates far too long, the Fed has created what Nassim Taleb would call a “fragile” market. By propping up financial institutions and asset prices, the Fed has pushed risk off into the future.

Note, they didn’t reduce risk; they simply moved it to a different place and let it compound. Rather than allow small, manageable fires, they have let fuel accumulate for a large fire. And then we will ask the arsonist to come in and put out the fire.

The coming volatile period is a direct result of Federal Reserve intervention in the workings of the market. They have now come to the place where they have to either let the fire of inflation (and a likely inflationary recession) or the fire of a recession and bear markets to erupt. Prior choices mean they have no good choices now.

The S&P 500 Index is less than 7% below its all-time, most-expensive closing price ever. It hit 4,796 on January 3, 2022. The index traded at more than three times sales then, its highest level in recorded history ‒ making it more expensive than it was at the 1929 and 2000 peaks. You know what happened next.

The risk in paying high valuations is not hard to understand. Valuation of any security is the value placed today on $1 of cash flow received in the future.

It’s easy to understand with bonds. If you pay $100 to receive $10 per year, you’re getting a 10% yield. It’s up to you to decide if that’s enough. If it is, you buy. If not, you pass.

It’s the same with stocks, only you don’t get interest payments. A stock is a piece of business, so a stockholder’s claim is on the future excess cash flows that the business generates.

We don’t know how much they’ll be or even if they’ll occur, which is why there’s generally more risk in stocks than in bonds.

We tend to see the wealth generated by securities as the price you pay to buy it at any given moment. But that’s wrong. The real wealth is in the cash flows. The share price is a current reflection of the market’s assessment about the size and certainty of those future cash flows.

The more you pay for those future cash flows, the lower your return will be. That’s simple, irrefutable arithmetic.

When you pay more than has ever been paid before, it’s only reasonable to expect a lower return than has ever been made. That can be true for a single stock or an entire index full of them.

The hard part about paying too much for stocks is that it can seem OK for a while. When prices keep rising, it tends to make folks think that valuations and even business fundamentals like profitability and financial strength don’t matter.

But over the long term, valuations and fundamentals become an inviolable law of nature, like the force of gravity… They are ultimately all that matters ‒ and investors who bet that way will survive.

Russian Sanctions

It has now been six weeks since Russia’s invasion of Ukraine, which has resulted in 1,563 confirmed civilian deaths, but likely thousands more. Western governments have promised to unleash the “mother of all sanctions” from the onset of the war, though it can be hard to keep track of all the penalties dealt to Moscow and its related entities. Here is a full list of U.S. sanctions since the start of the crisis:

February 24: Restricting exports of chips, computers and other high-end technologies to Russia.

February 27: Key Russian banks are blocked from SWIFT and sanctions are placed on the central bank’s international reserves.

February 28: Oligarchs are targeted with travel bans and asset freezes.

March 2: U.S. considers barring Russian ships from American ports.

March 8: Ban announced on Russian oil, gas and energy imports.

March 11: Move to strip Russia of its preferential trade status.

March 24: U.S imposes sanctions on dozens of Russian defense companies and the Duma legislative body.

April 5: Treasury stops the Russian government from paying holders of its sovereign via the dollar reserves it holds in American bank accounts. IRS suspends information exchanges with Russia’s tax authorities to hinder Moscow’s ability to collect taxes.

April 6: Sanctions unveiled against Putin’s adult children. All new investments are banned in Russia, while full blocking sanctions were imposed on Russia’s largest banks.

European governments are finally realizing their dependence on Russian natural gas creates big problems. Some want to stop buying, but that’s not an easy decision. The GZERO analysis outlines the arguments for and against.

Key Points:

- European leaders see strong public support for banning Russian fuel imports, even though they know higher energy bills will make voters unhappy.

- Russia sells about $373 million per dayto Europe and has few options to reroute those shipments elsewhere. Stopping it would be a big hit to Russia’s war machine.

- Individual country bans could create a domino effect even if the EU doesn’t act as a bloc.

- Banning Russian gas imports will increase the odds of European recession.

- Europeans losing jobs in large numbers could reverse the presently strong public support for helping Ukraine.

- Proposed new gas imports from the US and Qatar would fall way short of what Russia currently supplies.

Any gas Europe stops buying will most likely go to China at a steeply discounted price. So hurting one geopolitical foe may actually help another one. This is a situation with no good choices.

Market Data

- Small caps tend to outperform during periods of stagflation.

- Declining ISM manufacturing index and the Fed tightening monetary policy is not a good combination for stocks.

- The S&P 500 full 2022 earnings projections keep getting upgraded.

- The recent sharp increase in bond yields doesn’t bode well for earnings growth.

- Homebuilders are now down more than 20% vs. the S&P 500 over the past six months.

- The combined value of the five largest stocks makes up 24.2% of the combined total value of all the stocks in the S&P 500 Index.

- The top ten stocks make up 31.4% of the value of the S&P 500 Index

Quote of the Week

Those who dare to fail miserably can achieve greatly. –

John F. Kennedy

Picture of the Week

All content is the opinion of Brian J. Decker

{kind=link}

{kind=link}

{kind=link}