On a national basis, housing inflation has subsided significantly from a few years ago. Home prices and rental rates are even dropping a bit in some markets, and more than a bit in a few markets. But even in those places, costs remain higher—and often much higher—than they were before 2020.

This is where the discussion often gets confused. You see reports saying, “Home prices (or apartment rents) have stabilized.” That simply means they’ve stopped rising. This is good but not necessarily better.

Jim Bianco noted recently that housing is in perpetual crisis. When prices are rising, or stable at a high level, we have an affordability crisis. When prices are weak and/or falling, overextended homeowners fall behind on their payments, which can lead to a bank/financial crisis. Both conditions are self-correcting with time… but it can be a long time.

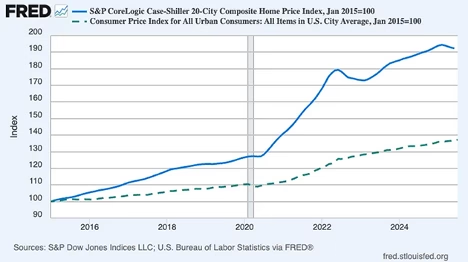

It’s hard to grasp how fast home prices accelerated over the last decade, relative to broader inflation. The chart below shows the Case-Shiller home price index vs. the Consumer Price Index since January 2015.

Source: Paul Krugman

In the five calendar years before COVID struck in 2020, home prices climbed almost 20 percentage points more than CPI headline inflation. Granted, CPI wasn’t rising much in that era, but home prices were definitely moving up (on a national average basis, with the large caveat that all real estate is local, etc., etc. And yes, I did just use a graph from Paul Krugman.)

Notice also how the home price index bent upward starting in 2021 when the Federal Reserve’s aggressive pandemic interventions produced sub-3% mortgage rates. The same thing happened, somewhat less aggressively, before 2020 and likely explains that price increase as well. Artificially low interest rates produce artificially high asset prices, whether for stocks, homes, or anything else. This is also one reason why the home price index briefly declined when the Fed hiked in 2022.

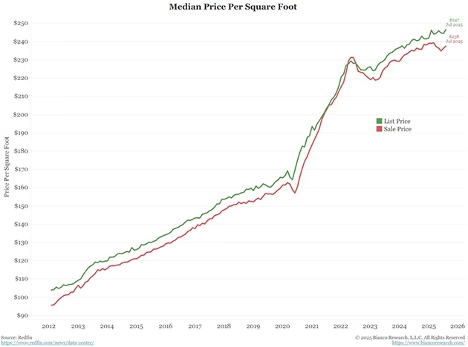

The same pattern is visible in this chart based on Redfin price data. This one is median price per square foot, so it accounts for changes in home size. Home prices rose steadily during the QE years, rose even faster in the COVID period, then resumed roughly the previous pace since 2022. On this square-foot measure, home prices have risen over 50% since 2020. Coupled with higher interest rates, it does indeed create an affordability crisis especially for first-time buyers.

Source: Jim Bianco

Home prices are relevant mainly to homeowners, or those who wish to buy a home. A large part of the population either prefers to rent or has to rent because they can’t find a suitable home in a suitable place at a suitable price.

Peter Boockvar, who somehow digests vast amounts of data almost as fast as ChatGPT, and generally has better conclusions, had this update on the rental market. (Emphasis mine.)

“Last week the August Apartment List National Rent Report, in case you missed it, said ‘The national median rent dipped by .2% in August, and now stands at $1,400. This was the first m/o/m decline since January and marks the beginning of the rental markets off season. It’s likely that we’ll continue to see further modest rent declines through the remainder of the year.’

“Versus last year, new rents are down .9%. The vacancy rate is at 7.1% which is the highest since Apartment List started this survey in 2017 and ‘We’re past the peak of a multifamily construction surge, but a healthy supply of new units are still hitting the market, and vacancies are still trending up.’ I’ll add, most of this supply comes from the sunbelt states with Austin, Texas, being the weakest market followed by Denver (not sunbelt but most others are), Phoenix, and Tucson. The best rental markets are on the coasts that have seen less supply growth. For example, San Francisco is now the best market with rental rates up 4.7% y/o/y, playing catch-up. Overall, ‘Units are taking an average of 29 days to get leased after being listed, up one day from last month’s reading, and down from a high of 37 days in January.’

“Not in this report but from what I heard from the publicly traded REITs, renewal rates are running at about 3–4% so the blended rental growth rate is about 1–2%. This is below what the CPI and PCE are telling us but again, keep in mind that CPI and PCE never captured the high growth rates seen in rents at the peak in 2022. [JM—As I have written many times, the way the BLS figures rent growth is a backwards-looking average number, so it will always be wrong at times of significant changes.] Also, while the rate of change in rent growth has clearly slowed, new rents are still up 22% from January 2021 and why consumer confidence levels for many are still at low levels with this being the biggest annual cost for those renting.

“The bottom line on where the rental market goes from here, Apartment List said, ‘With construction expected to slow further in the second half of this year and into 2026, conditions are likely to shift, but it will still take time for the market to metabolize the recent growth in the rental stock.’ I expect rent growth to stabilize in the first half of 2026 and expect rents to start rising again in the back half of 2026.”

I bolded Peter’s last sentence there because it’s key to where inflation is going. Any way you measure it, apartment rents are up substantially in many markets, to the great frustration of many workers—particularly young people. The growth has stopped in some places, but rental rates are still elevated, especially as seen from a year-over-year or even perhaps more important, over the last four years. Peter thinks this is only a pause and rates will resume rising next year.

I don’t know anyone who expects rental prices to fall much from here, short of a fairly severe recession (think the Great Recession) which of course we want to avoid. A mild recession historically has only modest impacts on prices over a year or so. Employment and wage growth are weakening, which at some point may force landlords to reduce rents, but the weakness would have to get quite a bit worse than we see now to really impact prices and rents.

Based on Jerome Powell’s Jackson Hole speech, a rate cut seems very likely this month. Getting ahead of rising unemployment seems to be the main goal, but some analysts think lower mortgage rates may be an additional benefit. That gives us two questions:

- Will lower rates at the short end of the curve also bring down mortgage rates?

- If so, will the lower rates make homes more affordable?

Let’s take those in order. Recent history suggests the first answer is “no.” Mortgage rates didn’t drop at all when the Fed cut rates this time a year ago. Has something in the last year changed the dynamic? Maybe. But the global trend in long-term interest rates is up, not down, and it’s hard to explain how the US would be different. Bond investors are increasingly concerned about inflation not just in the US but everywhere. Nothing large, mind you, just the beginnings of the trend. Something that you might expect, along with scores of other minor movements and trends, if we are moving towards a Great Reset by the end of the decade.

(Yes, long-term interest rates fell after Friday’s unemployment numbers. One day’s kneejerk move is noise. Ask me a month or so from now what the true effect was.)

For rates at the long end to drop, somebody needs to be willing to lend massive amounts of long-term cash at fixed rates. I don’t know who that will be. There’s no shortage of borrowers, i.e., governments. But they are issuing mostly short-term and floating-rate debt, and I suspect it’s because they know the demand for longer-term debt just isn’t there. Few investors are willing to take the inflation and other risks of writing a 30-year loan. That’s not unreasonable. A lot can go wrong between now and 2055.

That said, mortgages are different. The kind we have in the US, which gives the borrower an embedded prepayment option, exist in part because the government supports a market for them and in part because of normal market operations. If Congress, the president, and the Federal Reserve want those loans to be available on better terms, there are things they can do. It would have costs and side effects but might work for a while. As we have seen in the past, though, the long-term effects of those actions would at best be a serious market distortion.

The other question is stickier. Would lower rates make homes more affordable? They certainly help. The price is less important than the payment amount. Cutting two percentage points off a $300,000 mortgage reduces the payment by about $376 a month. Is that enough to entice a buyer who’s otherwise priced out? Maybe not, once they realize taxes and insurance are also substantial and, unlike a fixed mortgage, will likely rise each year.

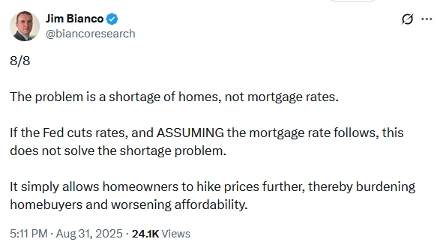

Lower mortgage rates alone would have limited benefit unless prices drop, too. Jim Bianco thinks home prices would actually rise to negate the benefit of lower mortgage rates.

Source: Jim Bianco on X

This is a supply and demand problem. Lower mortgage rates attack the demand side via reduced financing costs. They don’t magically put more houses on the market. Supply grows when builders decide to build more new homes and/or when current homeowners decide to sell. But in the latter case, the seller is usually a buyer, too. They have to go somewhere, so their decision adds to both supply and demand.

John Burns, who has forgotten more about housing than you or I will ever know, thinks lower rates will help, though not instantly. Reducing monthly payments will draw in enough new buyers to incentivize new supply. It will take time, but small differences add up.

In an interview this week, John also said remote work is also an underappreciated housing solution. If a company gives people the chance to work from home 2–3 days a week or even part time, then distance to the office becomes less important. This lets people disperse further to places where both houses and apartments cost less.

John also noted something surprising. There’s been a lot of speculation on the way immigration changes affect housing prices. In theory, if people are deported or leave the US voluntarily, it should create vacancies in the places they were living. That would have a downward effect on prices.

At the same time, there’s also concern about the loss of immigrant construction workers raising building costs. John’s firm works with literally hundreds of builders who say they don’t see widespread labor shortages. Stricter immigration enforcement so far seems to be having little effect on the construction industry.

The “lock-in effect” is gradually fading, too. People who got those sweet COVID mortgage rates are naturally reluctant to sell, but sometimes they have no choice. Death, new jobs, divorces, and other life events shrink the number of such homeowners.

Add all this up and there’s reason to think housing costs will come down over the next few years. This will help reduce inflation, but it’s going to be a slow process. Meanwhile, inflation seems likely to stay well above that “2% average” target the Fed used to follow.

Making the Fed decision even more uncomfortable will be the likelihood as I discussed previously that inflation will move up above 3% in the fourth quarter, making more than two rate cuts problematic. And it will get worse. After we quickly review the unemployment numbers, let’s ask the hard question that I suggested a few years ago might be a large problem in the future, which we may now just see the beginnings of: Has the Fed lost the narrative and control?

Great Quotes

“If you are going through hell, keep going.” – Winston Churchill

Picture of the Week

Gila Woodpecker

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}