Markets cheered a U.S.-Iran ceasefire, payrolls nearly tripled expectations, and tax refunds are running 14% above last year. On the surface, it looks like smooth sailing. But look closer and a more complicated picture emerges — Q1 GDP has been revised down to just 0.5%, part-time work is outpacing full-time employment for the third consecutive month, inflation remains well above the Fed’s target, and the rate cuts the market was counting on this year have quietly disappeared. At Decker Retirement Planning, we don’t manage your retirement around the headlines — we manage it around the data. Here’s what this week’s numbers actually mean for people heading into or already in retirement.

US Economy

The trade deficit widened. While exports rose to a record high, imports increased more on a month-over-month basis, driven by a surge in electronics and semiconductors for AI investment. The weaker net trade data prompted downward revisions to Q1 GDP tracking, lowering the Atlanta Fed’s GDPNow estimate from 1.7% to 0.5%. The downgrade was driven by further downward revisions to consumer spending, residential investment, and inventory accumulation.

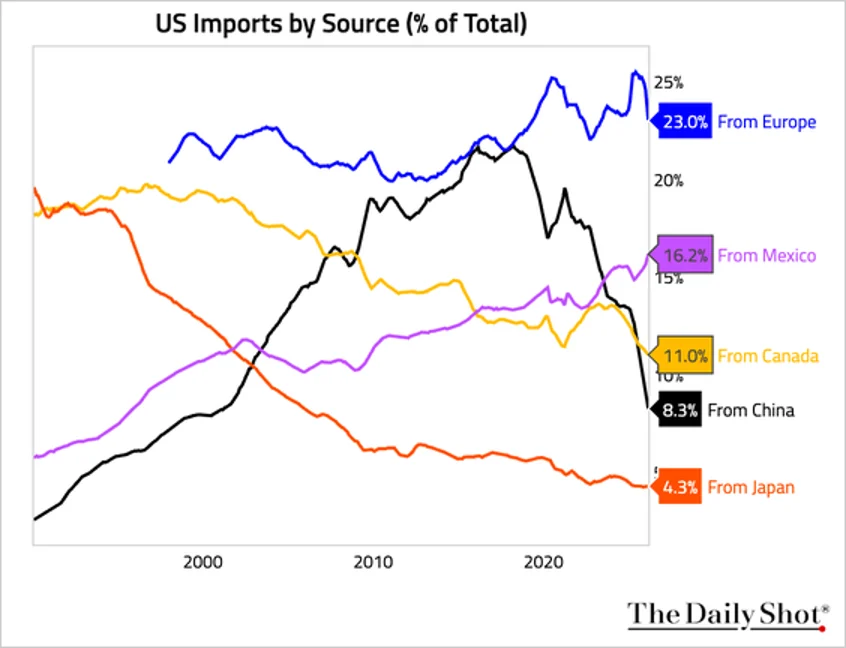

Direct imports from China as a share of total have fallen precipitously.

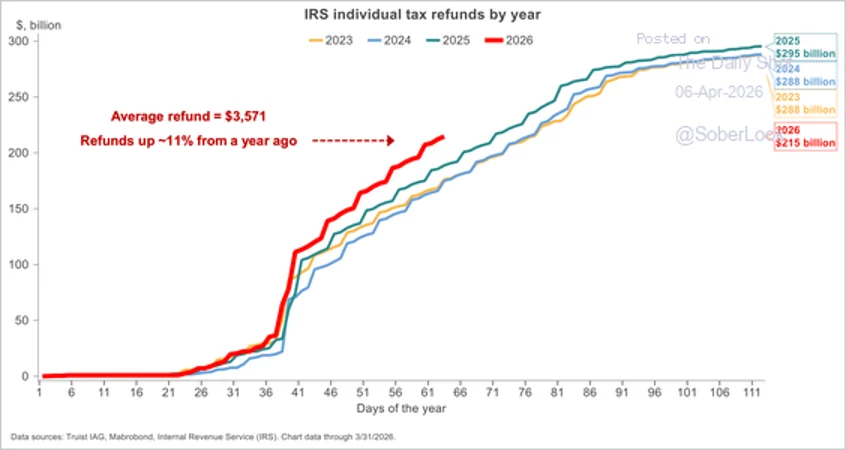

Tax refunds are running 11% ahead of prior-year levels, buffering the impact of higher oil prices.

Source: Truist Wealth

The services sector expanded by less than expected. The new orders index was the bright spot of the release, climbing to a three-year high and signaling some resilience in the demand pipeline.

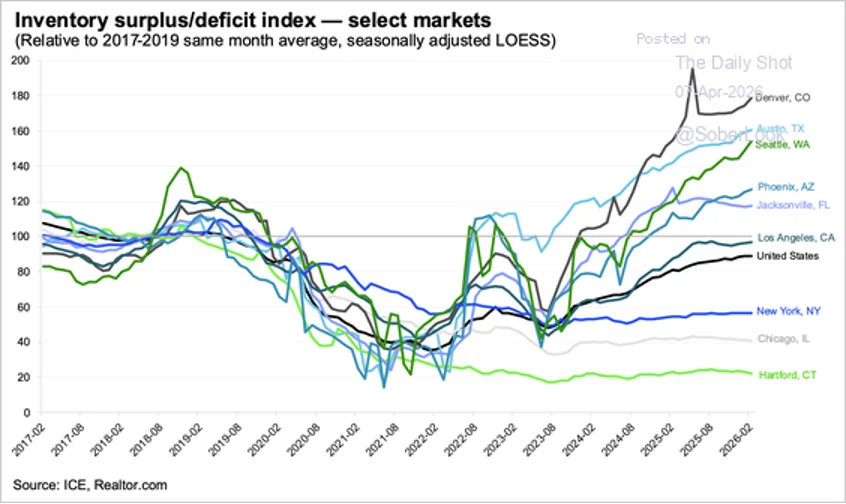

Housing inventory continues to improve nationally, but the pace is slowing. Denver, Austin, and Seattle have the highest inventory-to-sales ratio.

Source: ICE

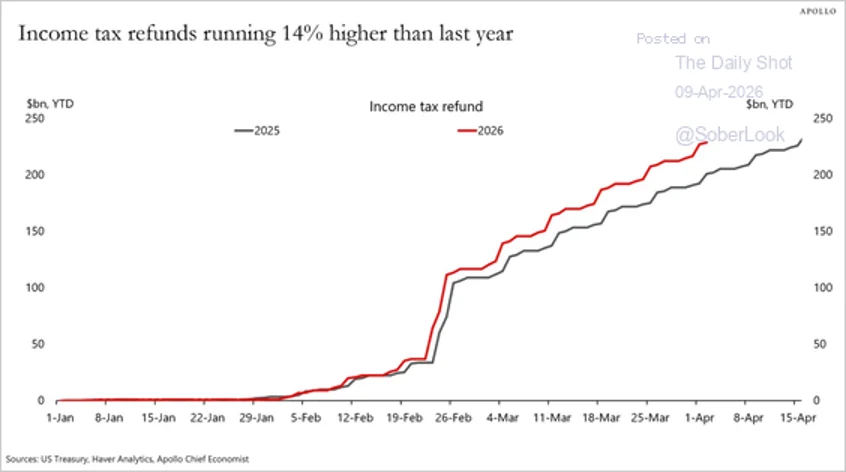

Income tax refunds are now running 14% higher than last year.

Source: Torsten Slok, Apollo

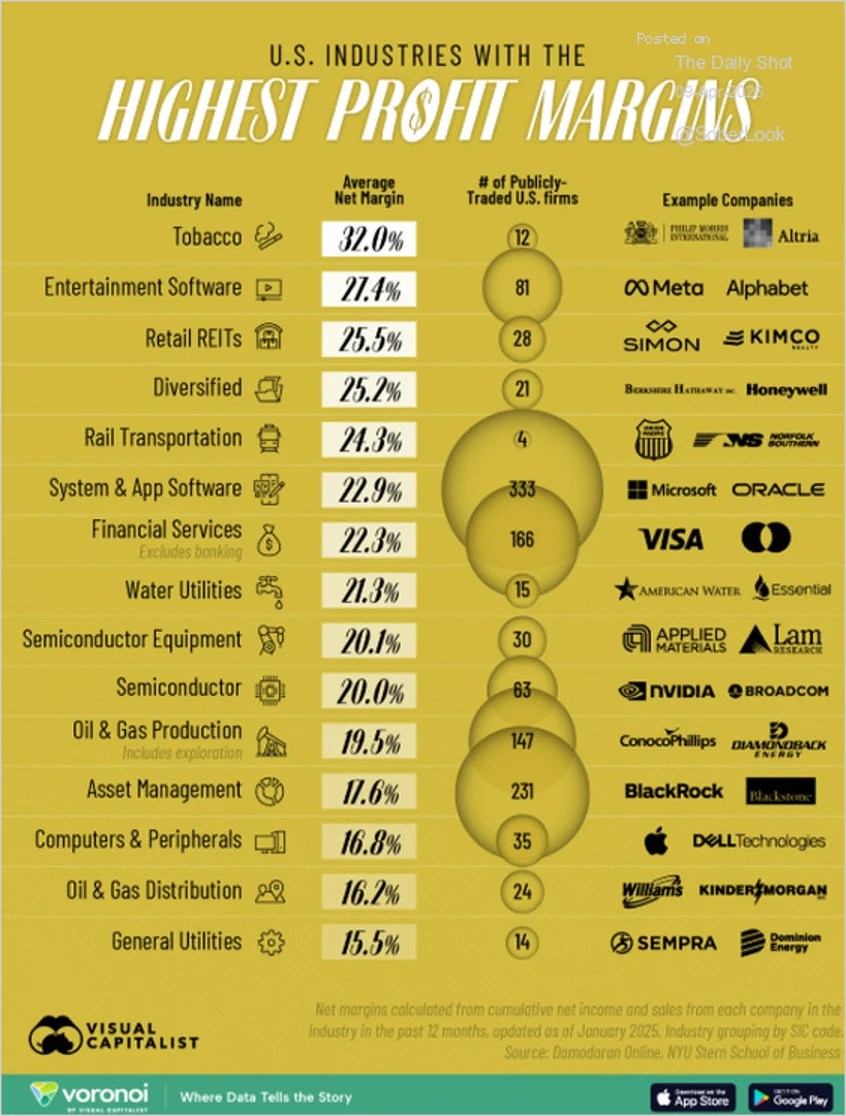

This chart shows the most profitable US industries.

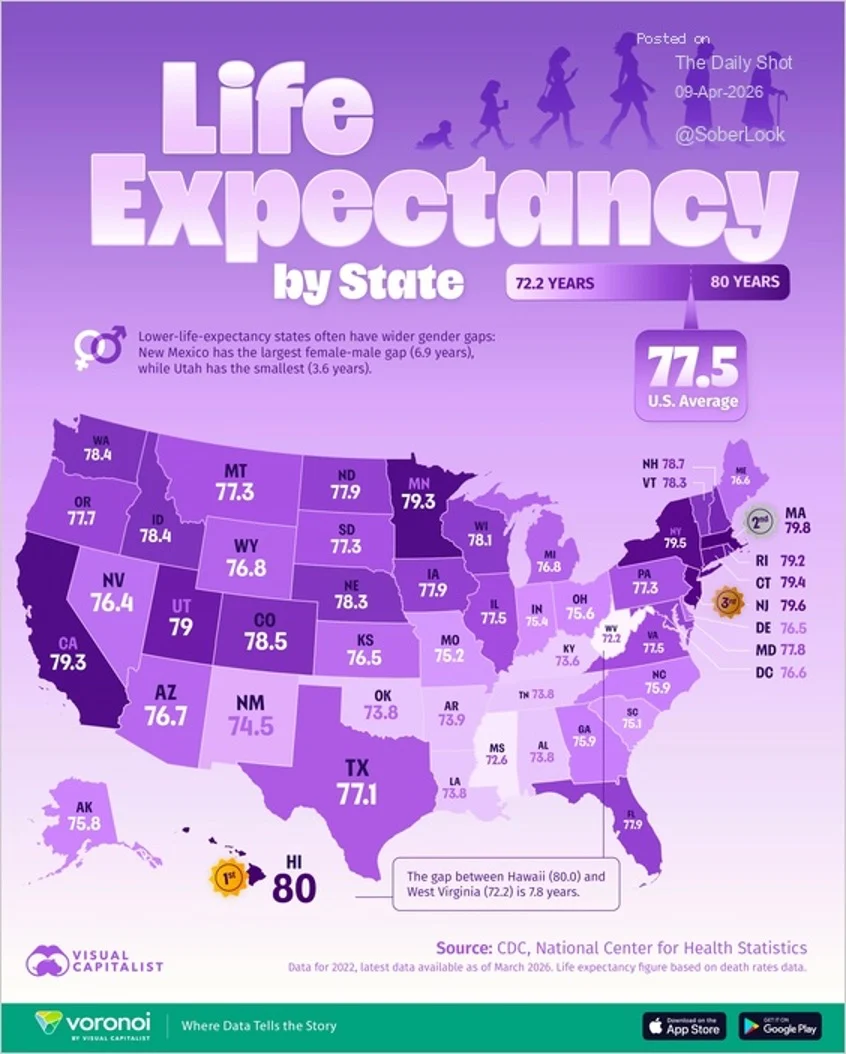

This map shows the life expectancy by US state.

Source: Visual Capitalist Read full article

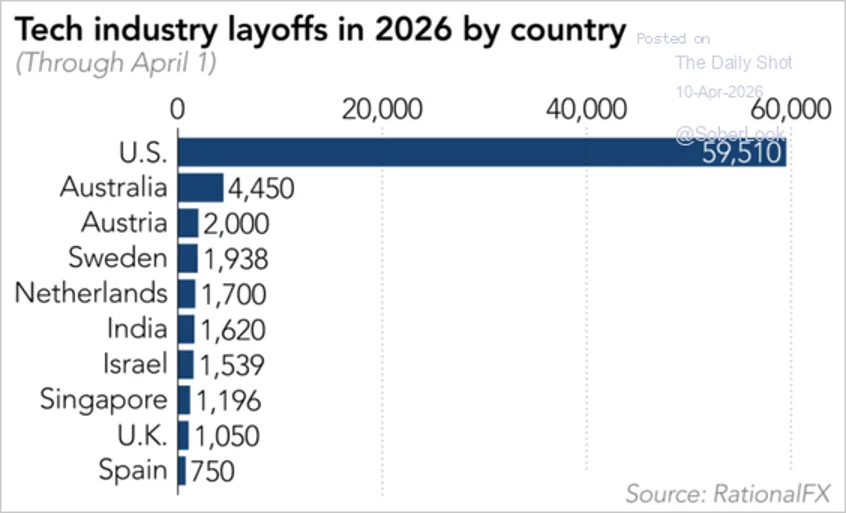

The US is leading in tech industry layoffs this year.

Source: Nikkei Asia Read full article

Look at the world’s most valuable companies. In 2010 just two of the top ten were “tech” companies. Now tech is 9/10!

These nine companies are worth a combined $22 trillion. Remarkably eight of them were founded in San Francisco or Seattle.

Jobs Report

Nonfarm payrolls jumped by 178,000 in March, almost triple the consensus estimate. Education and health services led the rebound, partially reflecting the end of the strike by healthcare professionals at Kaiser Permanente, which added back about 32,000 jobs. Leisure and hospitality employment also jumped, thanks to the return of more normal weather. The unemployment rate unexpectedly dipped by 10 basis points to 4.3%, below consensus. On an unrounded basis, the one-month decline in the unemployment rate was the largest since December 2021.

The decrease in the unemployment rate was primarily driven by a decline in the labor force. The underemployment rate (U6) actually ticked up. The spread between the year-over-year changes in full-time and part-time employment, which tended to fall below zero around recessions, has been negative for three consecutive months.

While hiring has been muted, there have not been many firings either. Initial jobless claims fell to 202,000, below consensus and near a two-year low, signaling limited layoffs. The four-week moving average fell for a sixth consecutive week. Continuing claims edged up, but remained lower than the same period last year.

Manufacturing employment has improved. Employment in the information sector continues to slide, with the cyclical peak coinciding with the release of ChatGPT. Wage growth for education and health services has fallen much more than that for the overall private sector.

At this point in the cycle, labor supply and demand are roughly in balance.

US Stock Market

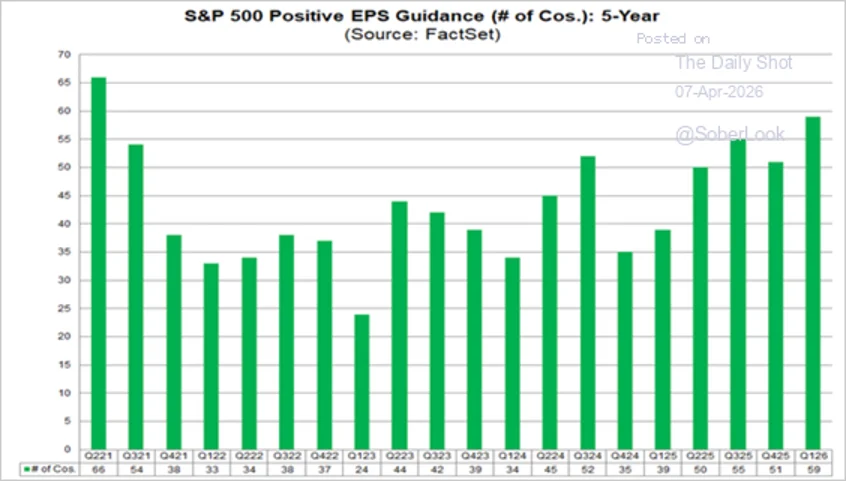

Growth in forward EPS has been accelerating. So far, 110 companies in the S&P 500 Index have issued Q1 EPS guidance, and 59 of them were positive. The percentage, 54%, is the highest in five years.

Source: FactSet

Oil prices fell sharply yesterday, with the decline concentrated at the front end of the futures curve. The term structure remains in deep backwardation, but prices are higher than pre-conflict levels across the curve.

Analysts slowed the pace of their upward earnings revisions but seem unconcerned about the impact of the energy shock on earnings. Consensus one-year-ahead revenue and earnings growth expectations are near multiyear highs, while long-term earnings growth has also remained elevated. We can also evaluate the evolution of growth implied by markets. One way to tease that out is to look at the relative performance of risk-matched stocks and bonds. By this measure, markets are now pricing in more growth than just before the Iran conflict began.

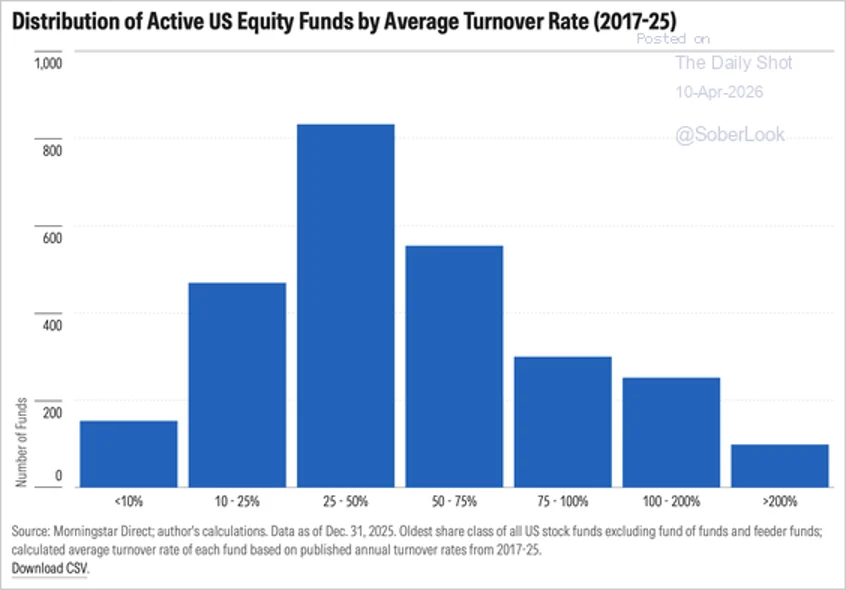

A typical active US stock fund manager turns over about half their portfolio each year.

Source: Morningstar Read full article

The War in Iran

The United States and Iran agreed to a two-week ceasefire contingent on reopening the Strait of Hormuz. Brent crude prices plunged, as did WTI crude prices. Gasoline prices plummeted. Global equities are rallying. Global bond yields tumbled. The US dollar depreciated, hitting a four-week low. Gold and silver rallied. Industrial metals gained as well.

The Fed

The March FOMC minutes show policymakers see two-sided risks from the Iran conflict. The “majority” of participants saw upside risks to inflation and downside risks to employment. “Many” participants judged that it would likely be appropriate to lower rates “in time” if inflation declined in line with their expectations, but the “vast majority” noted that progress toward the 2% target “could be slower than previously expected.”

Great Quotes

“The most important thing a father can do for his children is to love their mother.” – Elaine Dalton

Picture of the Week

Smiling red squirrel

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}