A look at the gap between gloomy consumer sentiment surveys and the spending, earnings, and labor data that tell a different story, and why the Michigan survey may be measuring something narrower than the headline suggests.

US Economy

The Philadelphia Fed’s manufacturing index rebounded. The composition of the report was strong, with shipments improving and new orders surging. Employment jumped back into expansionary territory. Price pressures were mixed, as prices paid by firms rose, while prices received fell, signaling potential margin pressure for firms.

Initial jobless claims edged down to 226,000. The four-week moving average rose, pointing to a potential, albeit modest, softening in the labor market. However, the overall level of claims remained low by historical standards. Continuing claims increased more than expected to 1.81 million but remained lower than during the same period last year. Leading indicators, such as the Challenger and WARN measure of job cuts, picked up modestly.

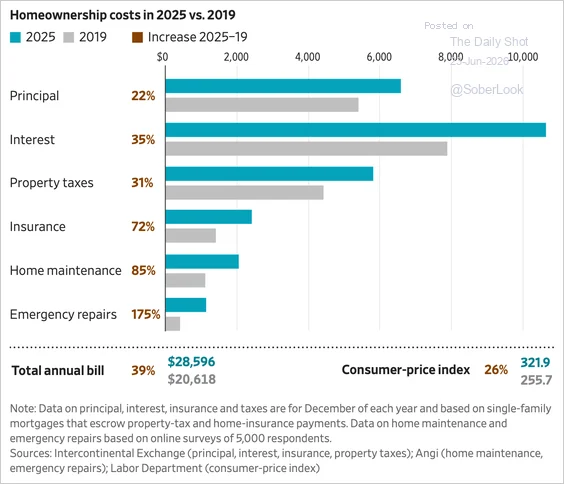

US 30-year mortgage rates fell to a one-month low. The total cost of homeownership has significantly increased since the pandemic.

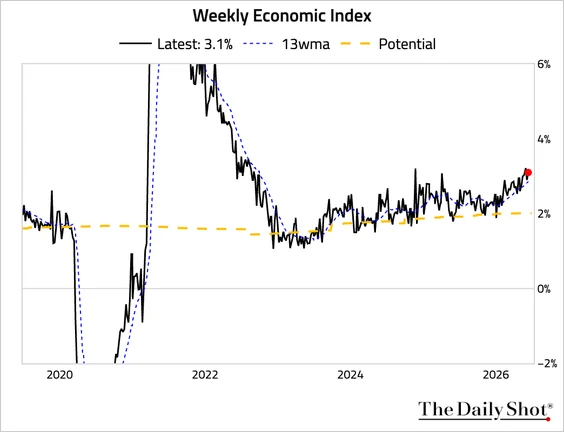

After the US–Iran agreement, Goldman cut the 12-month US recession probability to 15%, the long-term norm. The New York Fed’s DSGE model projects GDP growth to slow to 1.2% year over year in Q4 2026, while core PCE is forecast to remain stubborn, ending the year at 3.1%.

The Weekly Economic Index continues to signal strong growth.

Goldman’s Current Activity Indicator (CAI) for the US also shows solid growth at 2.5% in June. The Redbook index of same-store sales growth accelerated to its highest level since late 2022. The S&P Global manufacturing PMI rose to the highest level in more than four years, as output and new orders strengthened, although much of the gain reflected inventory building. The services PMI improved modestly.

The Q1 GDP growth rate was revised up to 2.1% (Q/Q SAAR) from a second estimate of 1.6%.

US Stock Market

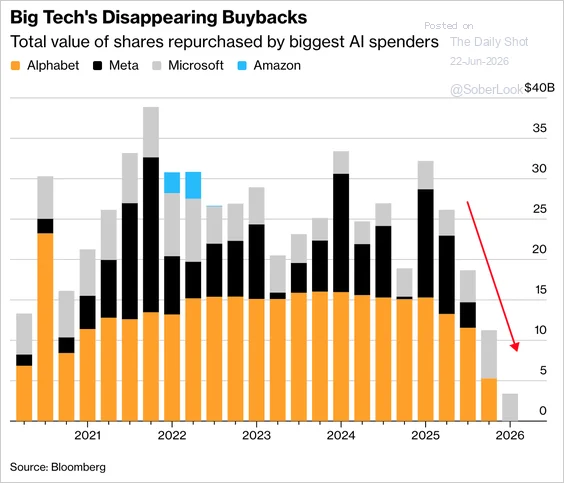

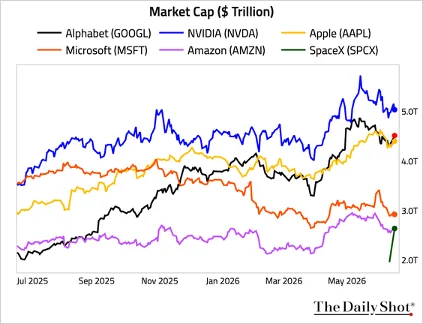

Surging AI capital expenditures are displacing Big Tech share buybacks, with only Microsoft repurchasing stock in Q1 among the four largest AI spenders.

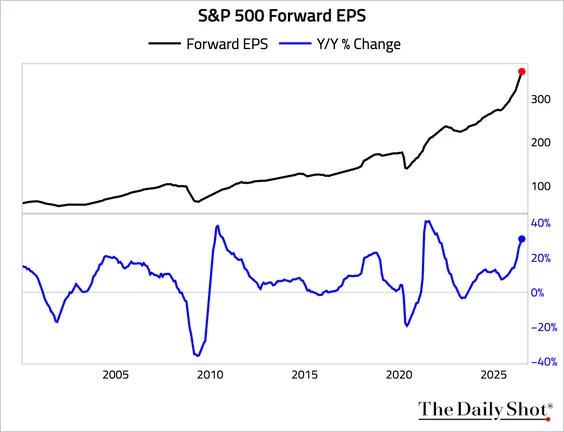

Growth in forward EPS has been accelerating.

What are the top 10 leadership qualities linked to high-performing companies?

The year-to-date return of the Russell 2000 (Small Caps) is the strongest since 1991. Expectations are for semiconductor earnings to grow another 35% in 2027 after a massive 117% expansion in 2026.

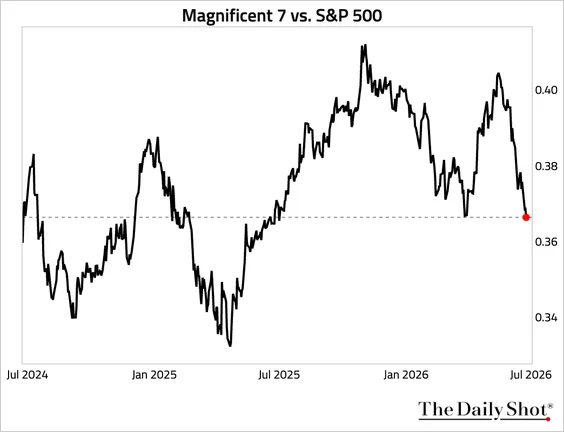

Magnificent 7 stocks continue to underperform the broader market.

US Stock Market

The S&P 500 Equal Weight Index has reached its 25th record high in 2026. The ratio of small-cap to large-cap equities has reached the highest level since December 2024. Consumer discretionary continues to weaken relative to the broader market, with the relative ratio sinking to 2012 lows. Momentum stocks continue to outpace the overall market.

The Russell 2000 has outperformed the S&P 500 by about 15% over the past year. Small-caps continue to lead the recovery in market breadth.

SpaceX’s valuation continued to surge.

The Fed

The June FOMC statement was the second shortest since 2007.

Great Quotes

“There are only two ways to live your life. One is as though nothing is a miracle. The other is as though everything is a miracle.” – Albert Einstein

Picture of the Week

Branick Castle, Slovenia

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}