In the next few weeks, the U.S. central bank will accelerate its plans to “digitize” the U.S. dollar.

You see, most people are so used to their PayPal and Venmo apps for moving money in a few seconds that they’ve forgotten that banks take days to actually clear the funds.

Sure, those apps may feel instant. But what’s really going on is that banks are covering the transfers out of their own pockets while they wait for your money to move from one account to another. That shields users from inconvenient delays, but it puts them at the mercy of big corporations with control over our transactions.

On July 1, the Fed will release a new instant-money platform called FedNow, and it will affect every American with a bank account.

The U.S. Treasury and Social Security Administration will begin using it and 120 banks have already signed up to do the same. And it could spell the end of centralized money-transfer apps like PayPal and Venmo.

Soon after the launch of FedNow, we expect to see an increase in all online and digital transactions and the government’s digital dollar will bring with it more influence on our lives than most people can imagine.

In time, blockchain and digital wallets will become the only technology capable of protecting everyone’s digital dollars while we enjoy instant transactions 24 hours a day, seven days a week.

Now, some may think a digital dollar will inevitably lead to less privacy for everyday people and that this is another example of government overreach. Others believe the launch of FedNow actually could represent an opportunity for more privacy and a drive a boost in demand for cryptocurrencies and the technology that underpins them.

I watched what happened in Canada when the truckers went on strike and the Government in Canada froze their bank accounts. The Government has access.

That’s what I worry about.

US Economy

- The Q1 GDP growth was revised sharply higher, …

- … boosted by trade and consumer spending.

- Initial jobless claims unexpectedly declined last week. Some analysts suggested the drop was just noise and that unemployment applications will rebound in the weeks ahead.

- Layoff indicators keep trending higher.

- The Citi Economic Surprise Index surged this week.

- Fed officials are talking about two more rate hikes.

Source: @Jonnelle

- July looks like a done deal. Could we see another increase in September or November?

- Initial jobless claims remain elevated compared to pre-COVID levels as well as 2022.

- Existing home sales remain depressed but were slightly above forecasts last month.

- US manufacturing activity deteriorated this month, according to S&P Global PMI. Factories are reporting falling orders.

- Service firms continue to report expansion, …

- with business expectations rebounding.

- Service companies still face strong inflationary pressures, but fewer firms boosted prices this month.

- The Conference Board’s index of leading indicators declined again in May.

- The Dallas Fed’s manufacturing index continues to show persistent weakness in the Texas-area factory activity.

- Demand has been deteriorating.

- Factories are now cutting sales prices.

- Companies are reducing workers’ hours.

- However, manufacturers are becoming more upbeat about the future.

- Homeowners have secured exceptionally low mortgage rates and remain largely unaffected by the recent surge in rates.

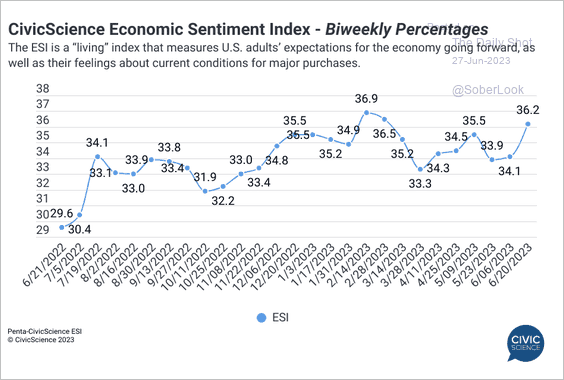

- The Conference Board’s consumer confidence index climbed in June, topping expectations. The report confirmed the latest gain in the Penta-CivicScience index (see chart from yesterday).

- The labor differential indicator (“jobs plentiful” less “jobs hard to get”) moved higher, suggesting that consumers remain confident about the job market.

- Durable goods orders unexpectedly jumped in May, boosted by transportation.

- New home sales surged in May (up almost 26% vs. 2022).

- Existing home prices were down on a year-over-year basis in April.

- Mortgage applications have stabilized at multi-year lows.

Market Data

- The Nasdaq 100 valuation continues to diverge from real yields. Something has to give.

- Almost 90% of the Treasury curve is inverted.

- JPMorgan Asset Management expects global economic divergence, with the US slowing and the rest of the world improving.

- The Nasdaq 100 is highly concentrated.

- Profit margins continue to face persistent downside risks.

- The S&P 500 risk premium is nearing the 2007 lows. This trend does not bode well for the market’s longer-term performance.

Quote of the Week

“Look for something positive in each day, even if some days you have to look a little harder.” – Unknown *** Brian here. This has been HUGE in my life!!

Picture of the Week

Sedona, AZ

All content is the opinion of Brian Decker

{kind=link}