The S&P 500 just closed at a fresh all-time high. Profit margins are at their highest level since FactSet began tracking in 2009. Earnings are growing at 15% year-over-year, and analysts keep raising their 2026 numbers. By every traditional measure, this is what a healthy market looks like. So why am I cautious? Because more than 70% of the increase in 2026 earnings estimates is coming from just six companies. The index is trading at a 42% premium to the rest of the world. And within weeks, the Federal Reserve will hand the chairmanship to Kevin Warsh — a man whose reaction function not a single trader on Wall Street has yet calibrated. Strong earnings late in a cycle aren’t a buy signal. They’re a description of what’s already happened. Here’s the setup I’m watching, and why it matters for the way we’re managing risk heading into summer.

US Economy

The University of Michigan consumer sentiment index fell to a record low, despite the upward revision. Both the current conditions and expectations components were revised higher.

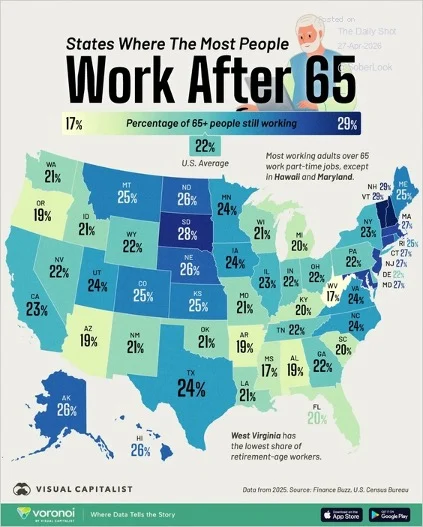

This map shows the percentage of Americans who continue to work after turning 65 by state.

The number of empty crude supertankers headed to the US to load has surged.

![]()

What was the top export in each state?

US Stock Market

Only 3% of companies have lowered guidance this season, well below the 8% average across the more than 90,000 reports tracked by Bespoke over the past decade.

Let’s begin with some updates on earnings and valuation.

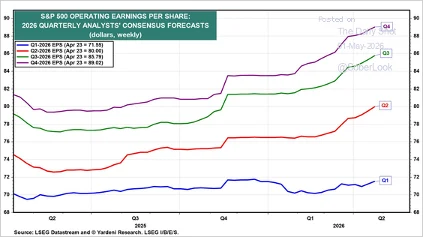

Analysts continue to raise their EPS forecasts for 2026.

Source: Yardeni Research

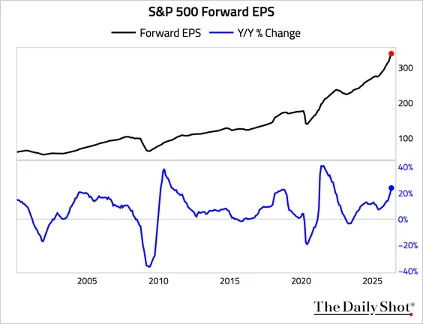

Growth in forward EPS accelerated.

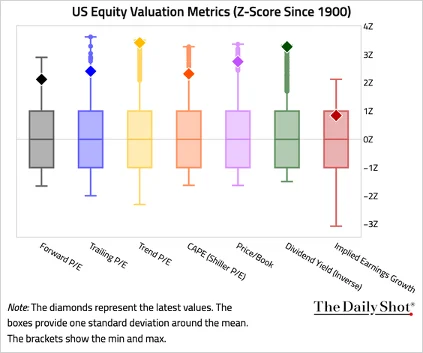

This chart summarizes US equity valuation metrics since 1900. Nearly all measures are near or over two standard deviations away from the long-term mean.

S&P 500 forward P/E has rebounded and remains elevated.

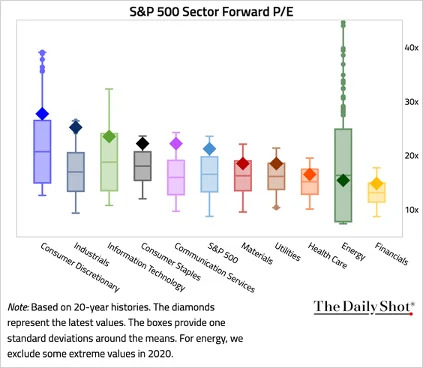

Here’s an overview of S&P 500 sector forward P/Es, summarized over the past 20 years.

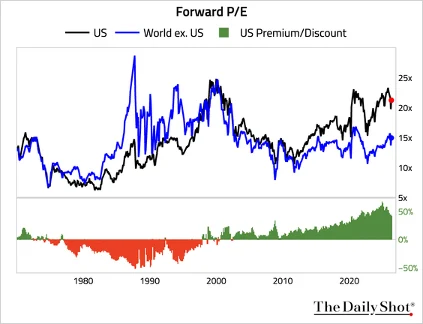

US equities are trading at a 42% premium relative to the rest of the world.

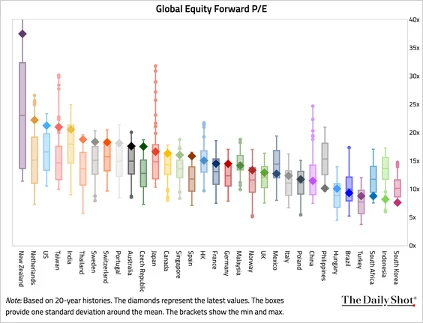

Here’s global equity valuation by country.

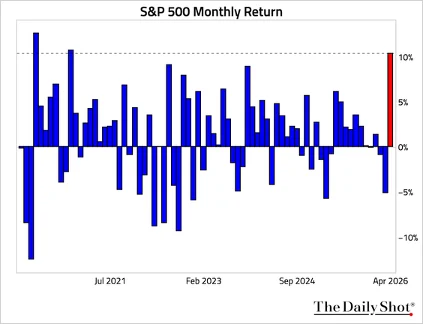

The S&P 500 posted its strongest monthly gain since 2020.

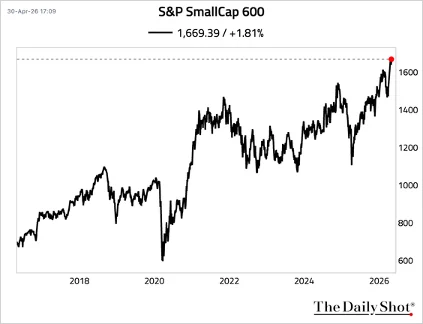

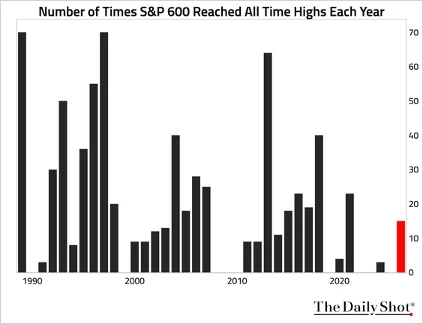

S&P SmallCap 600 has reached record highs 15 times in 2026.

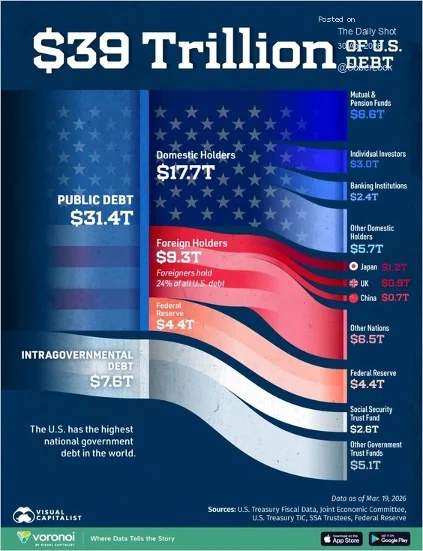

Who owns America’s debt?

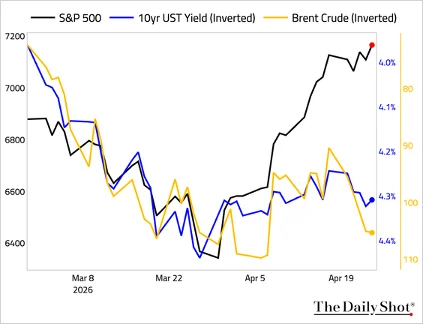

Equities have decoupled from the price action of bonds and oil.

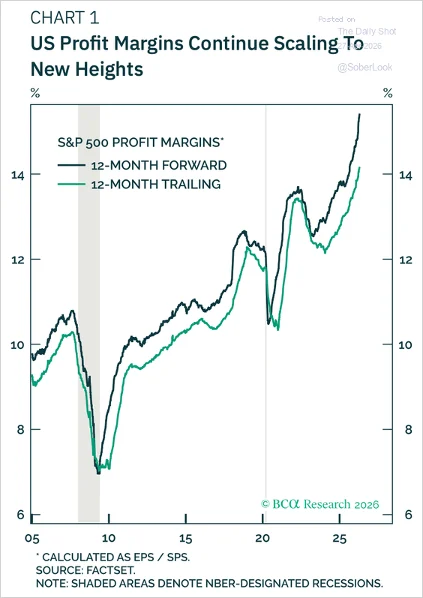

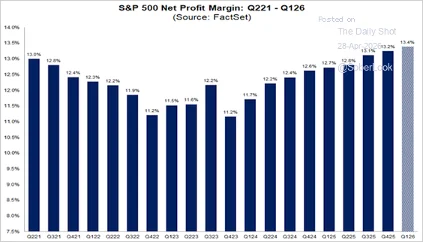

Both trailing and forward profit margins are surging to new highs. Energy and IT have been the main drivers of upward revisions to earnings and sales estimates.

The S&P 500 is on track to record its highest Q1 net profit margin since 2009.

Source: FactSet Read full article

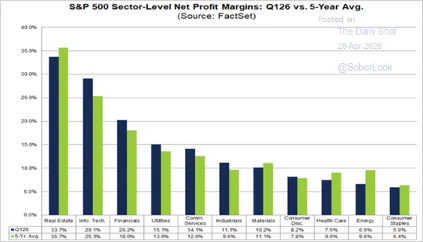

This chart shows net profit margins by sector.

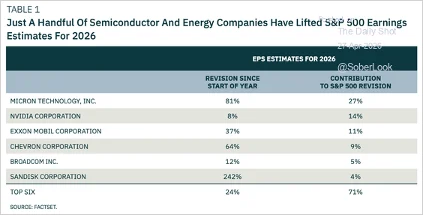

More than 70% of the increase in 2026 EPS estimates comes from just six companies, benefiting from a shortage of oil and semiconductors, according to BCA Research.

Source: BCA Research

The top 10 public companies are now worth more than the total GDP of G7 countries (excluding the US).

The Fed

The FOMC kept the Fed funds target range unchanged at 3.5%–3.75%, as expected. Governor Stephen Miran dissented again in favor of a 25 bps cut, while Presidents Beth Hammack, Neel Kashkari, and Lorie Logan soft dissented by not supporting the “inclusion of an easing bias in the statement.” This is the highest number of dissents in a single meeting since 1992. Revisions to the statement were modest. Job gains are now deemed to “have remained low, on average,” rather than just “remained low,” acknowledging the March pickup in payrolls. Inflation is “elevated” instead of “somewhat elevated,” and only “in part” due to the rise in energy prices. Chair Powell said he will remain at the Federal Reserve as a governor after his chair term ends.

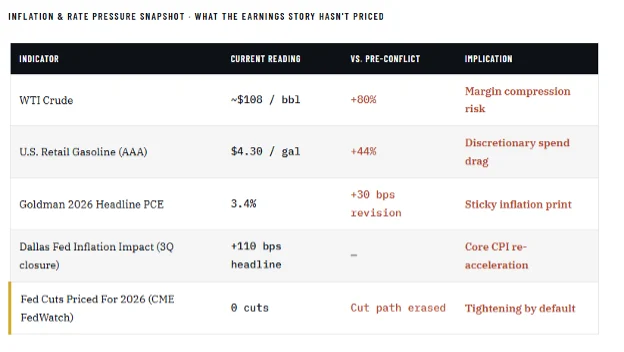

Consumers’ median inflation expectations over the next year were revised down by 10 bps to a still elevated 4.7%, while the longer-term expectation was revised higher by 10 bps to 3.5%. CPI fixings for the rest of the year imply materially higher inflation than before the Iran conflict began due mostly to energy prices.

Powell’s term ends in May. That is not a future risk; that is happening this month. The market has been so focused on the cut-versus-hold debate that it has paid almost no attention to how Kevin Warsh will respond when the next inflation print lands. Unfortunately, Warsh inherits the most awkward set of conditions any Fed chair has faced in a generation: headline inflation potentially re-accelerating into the third quarter, equity markets at all-time highs with margins already at record levels, and a fiscal backdrop that gives the central bank zero room to accommodate a slowdown. There is no version of the next chair’s first six months that goes quietly.

The deeper issue is the reaction function. Powell’s framework is known. Traders have spent four years calibrating their models to how he weighs employment versus inflation, when he leans on financial conditions, and how he uses the dot plot. Warsh starts that calibration from zero. The first FOMC meeting under new leadership will be the highest-stakes communication event of the year, and the market historically struggles with reaction-function uncertainty.

The transition pattern itself is worth noting. Major leadership transitions at peak valuations have a checkered historical record. Welch to Immelt at GE. Gates to Ballmer at Microsoft. Greenspan to Bernanke in February 2006, just as the housing market was peaking. Apple’s announcement Thursday of a Cook-to-Ternus CEO transition slots into the same pattern. Two of the most consequential leadership handovers in markets, at the largest stock in the index and the central bank that sets the global cost of capital, are happening within weeks of each other, with the index trading above 21x forward earnings on consensus estimates that history says are too high. That is not a forecast. It is a description of where we sit.

An index priced for 18% earnings growth, against a Fed reaction function nobody has calibrated yet, is a setup for disappointment from both directions. If Warsh signals continued restraint, equity multiples have to absorb a higher-for-longer message that is not in the price. If he signals premature accommodation, the inflation trade reignites, and the long end of the curve does the tightening for them. There is no clean path through the next six months.

Great Quotes

“If you want to know what a man’s like, take a good look at how he treats his inferiors, not his equals.” ― J.K. Rowling

Picture of the Week

Green-headed tanager (Tangara seledon), Brazilian wildlife and birdwatching

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}