The Federal Reserve held rates steady and Chair Powell signaled that cuts are off the table until inflation shows clear progress — and with February PPI jumping 0.7% and core services inflation breaking above its two-year range, that progress isn’t here yet. Q4 GDP was revised down to 0.7%, sentiment is at a six-month low, and oil remains elevated. Here’s what this week’s data means for your retirement portfolio.

US Economy

Q4 GDP growth rate was revised down sharply to 0.7% (Q/Q SAAR) from an initial estimate of 1.4%. The downgrade was driven by weaker-than-previously-reported consumer spending (particularly health care spending), business investment, government spending, and net trade (revised to a drag).

Stripping out government spending, net trade, and inventories, growth in real final sales to private domestic purchasers was revised down by 0.5 percentage points to 1.9%, the weakest reading in three years. Looking beyond Q4, personal income growth rose in January, but slightly less than expected.

Nominal personal spending increased by 0.4% month over month, slightly above expectations. Durable goods orders were unexpectedly flat in January, significantly missing the consensus forecast for a solid gain. The weakness was driven primarily by a drop in defense aircraft orders. Stripping out transportation, orders rose by a modest 0.4%, though that’s still slightly below consensus. Core capital goods orders, a proxy for business investment, were roughly flat, signaling a soft start to Q1.

Shipments of computers and electronic products continued their solid expansion. Job openings rebounded by more than expected.

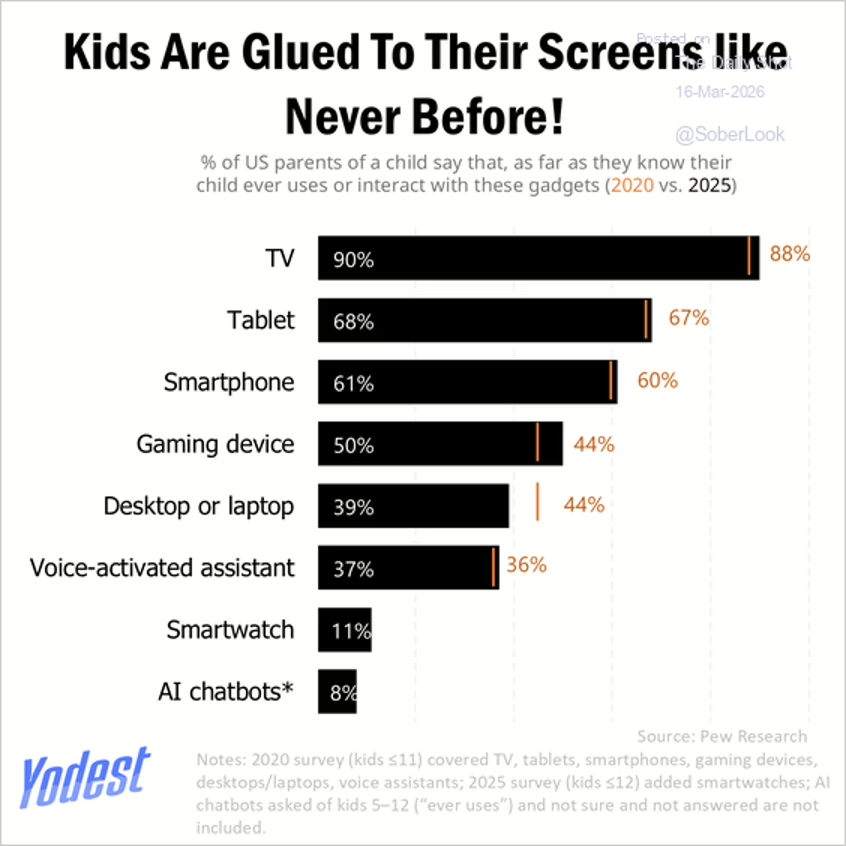

What gadgets are American kids using? 2020 vs. 2025.

Source: r/charts Read full article

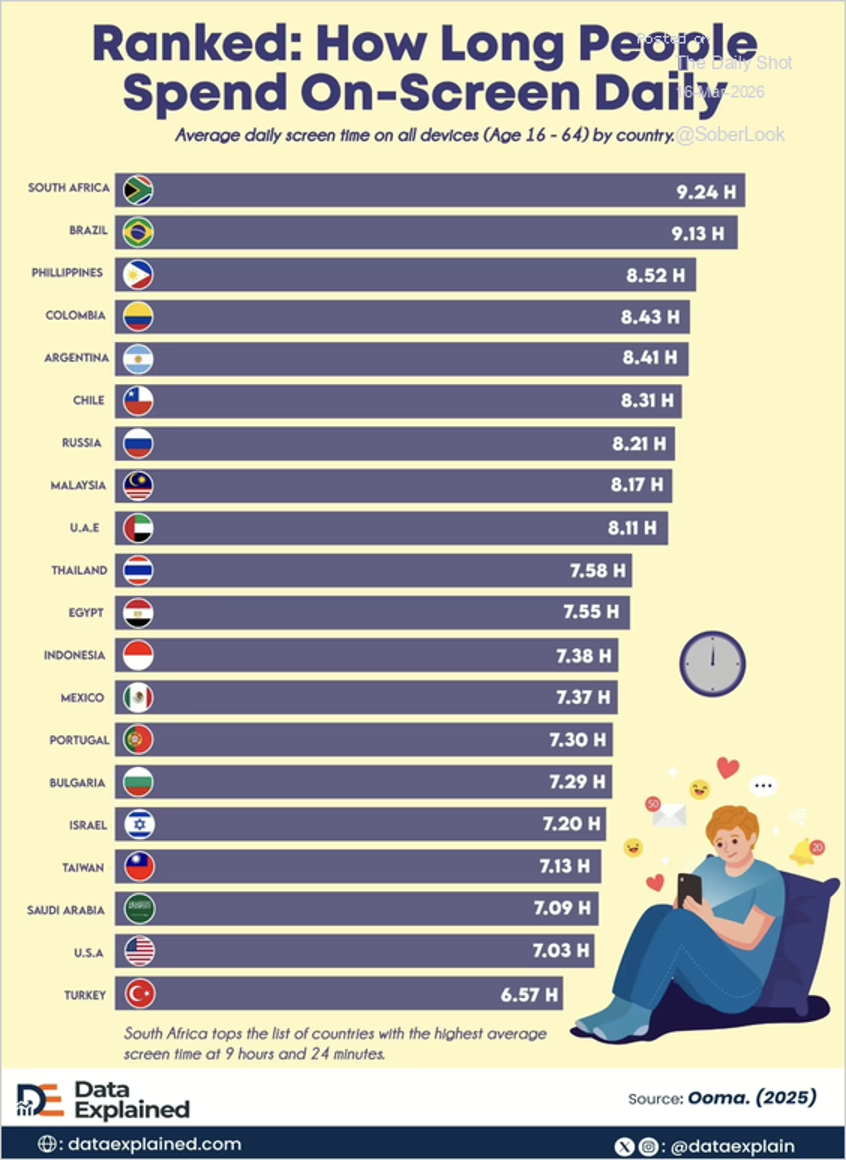

2. How long are people spending on screens daily?

Source: Visual Capitalist

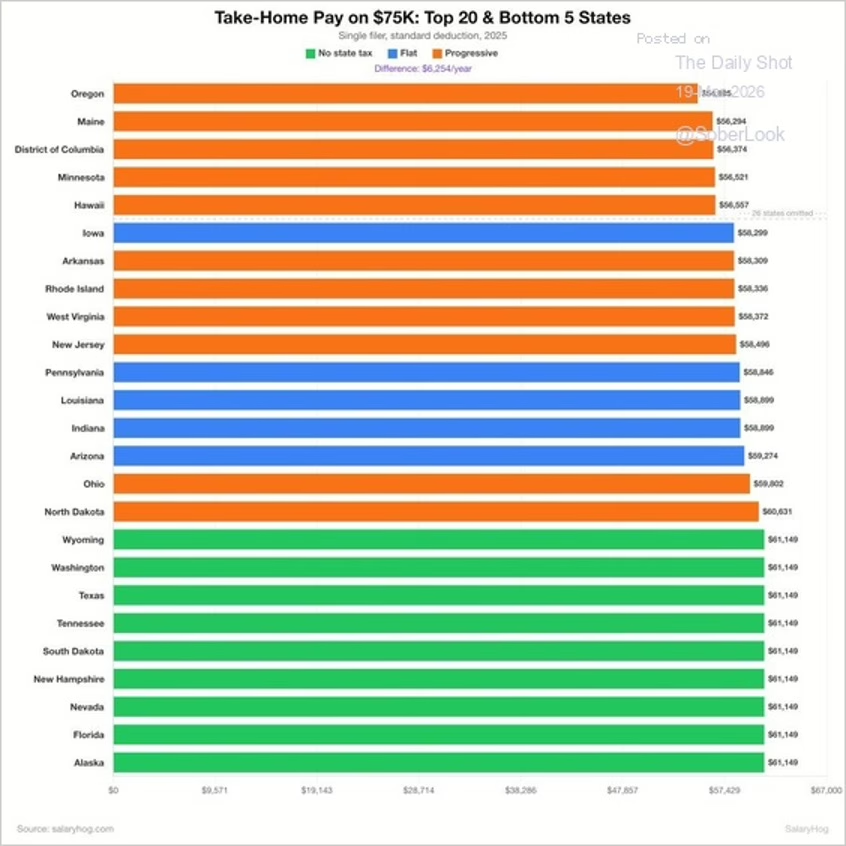

This chart shows your take-home pay on a $75k salary across various US states.

US Stock Market

According to BofA’s fund manager survey, investor sentiment fell to a six-month low. Cash levels jumped by the most since March 2020. Fund managers remain underweight US equities,

but have increased allocation to EM equities. Investor sentiment is rotating toward defensive sectors. US equity performance has shifted toward companies that pay dividends.

However, seasonality points to a stronger US market. The S&P 500 is entering a seasonally strong period.

Source: Paradigm Capital

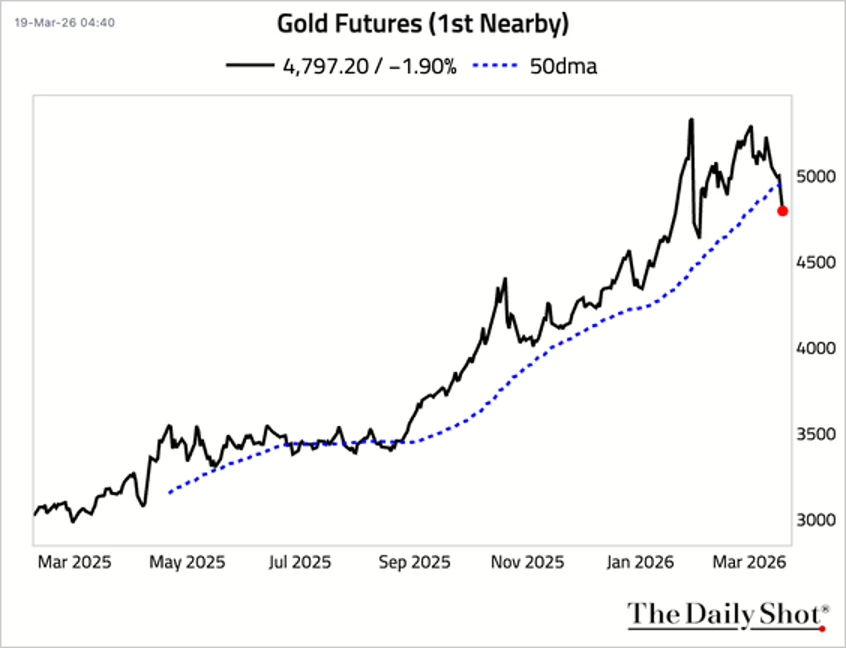

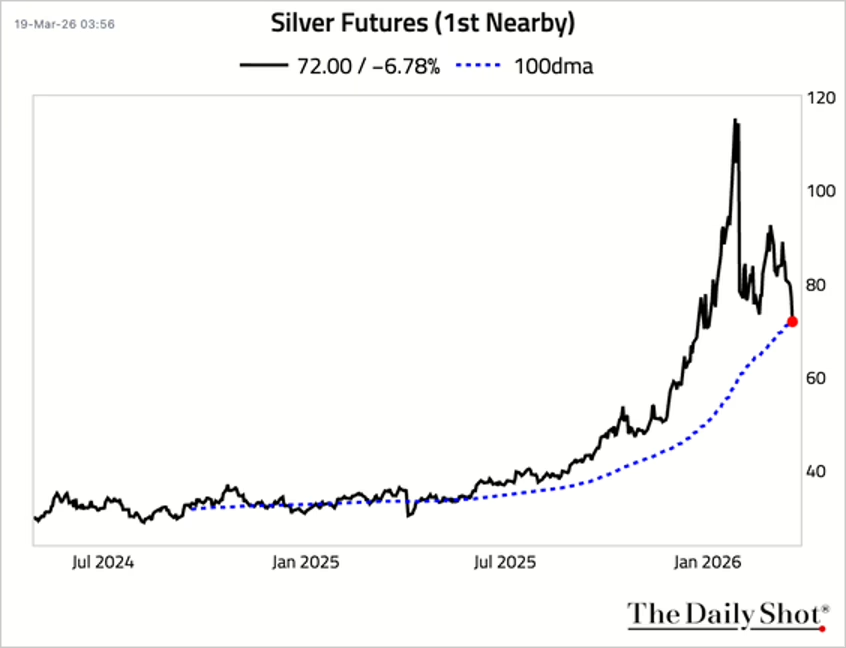

With expectations going to zero for Fed rate cuts this year, the US Dollar has started to rise and Gold and Silver starting to fall:

Gold fell below its 50-day moving average.

Silver fell below its 100-day moving average.

The Fed

The FOMC kept the Fed funds target range unchanged at 3.5%–3.75%, in line with consensus. Governor Stephen Miran dissented in favor of a 25 bps cut, bringing the total dissents this year to three. The FOMC statement now characterizes the unemployment rate as “being little changed in recent months” rather than “[having] shown some signs of stabilization,” which suggests less confidence in the state of the labor market. The statement also adds that “The implications of developments in the Middle East for the U.S. economy are uncertain.”

Chair Powell signaled that further rate cuts are not assured, conditional on clear progress on inflation. He also noted that there was “meaningful” movement toward fewer cuts among participants and that some talks had surfaced about the possibility of the next move being a rate hike. Markets reacted hawkishly to the remarks.

The dollar strengthened, which also means that Gold and Silver fell.

February’s headline PPI jumped by 0.7% month over month, while core PPI inflation rose by 0.5%, both well above consensus estimates, signaling firm upstream inflation pressures even before the recent oil-driven supply shock.

Expectations for a Fed rate cut in 2026 went to almost zero.

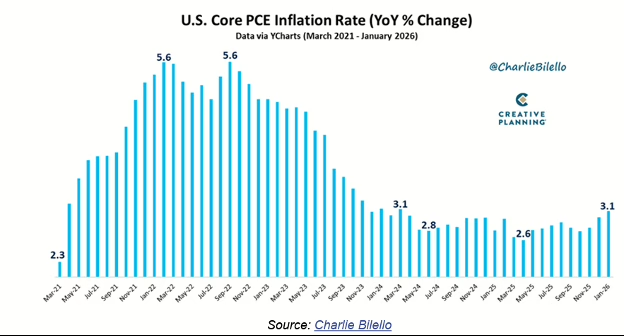

When Federal Reserve officials talk about their 2% inflation target, they mean inflation as measured by “Core PCE.” That’s the Personal Consumption Expenditures index, minus food and energy. The chart below offers some perspective on this benchmark.

Core PCE was running at a 2.3% annual rate as the COVID crisis receded in early 2021. It climbed quickly from there, reaching 5.6% in 2022 thanks to both supply chain pressures and the Ukraine war. By mid-2024 it was below 3% again but remained stubbornly above the 2021 level. The most recent data covering January 2026 shows Core PCE back above 3%. There is no sign it will fall to the Fed’s 2% target. Reaching that level would likely require a severe recession… which of course no one wants to see. But with the target still at 2%, recession would appear to be the Fed’s implicit goal.

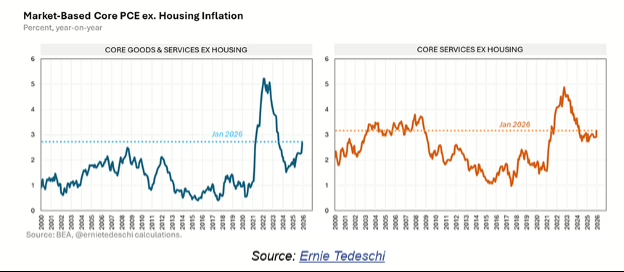

The charts drill into the PCE data to remove the impact of housing prices. Inflation data (both CPI and PCE) considers housing a “service” and not a “good.” This data shows services inflation rising even if you ignore housing prices.

The right chart shows core services ex-housing recently broke out of the two-year range between 2.7% and 3%. It is now 3.2%. The left chart adds core goods to the picture, minus housing. This kind of inflation (not counting food, energy or housing) is rising at 2.7%, the highest since year 2000. Worse, it’s climbing quickly. Inflationary forces seem to have embedded themselves deeper into the economy, even before any impact from the Iran war.

Iran and World Oil

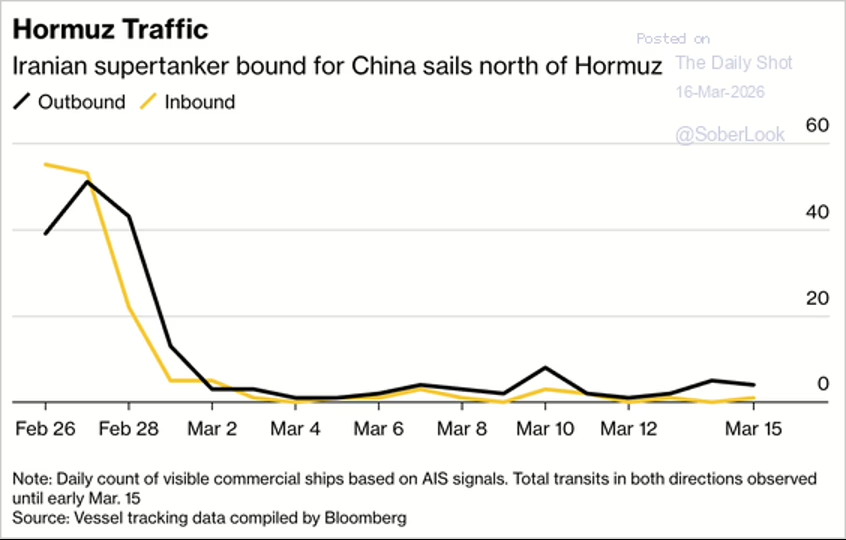

Commercial shipping through the Strait of Hormuz remains extremely limited.

Source: @markets Read full article

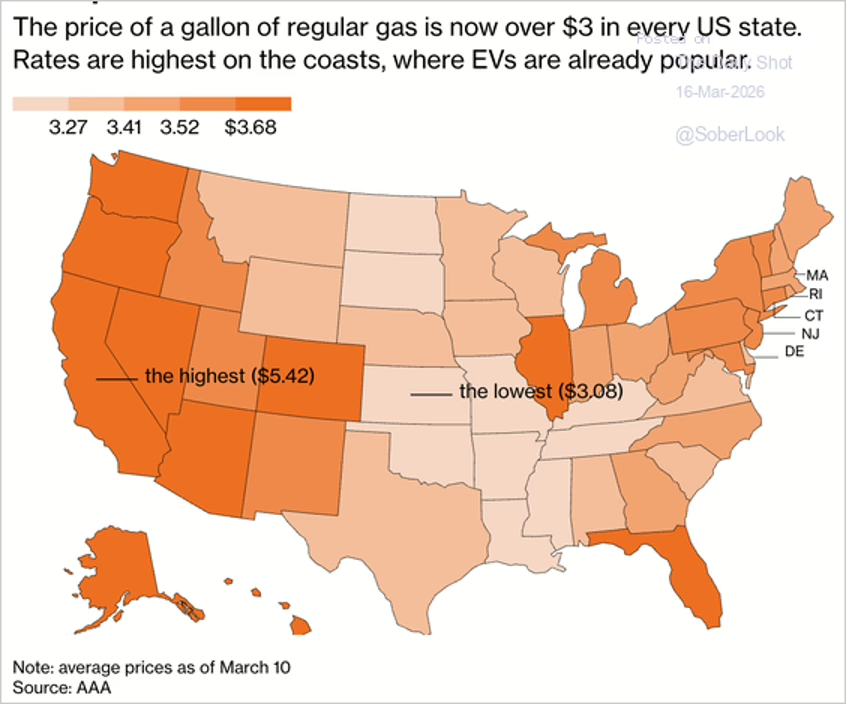

The price of a gallon of regular gasoline is now over $3 in every US state.

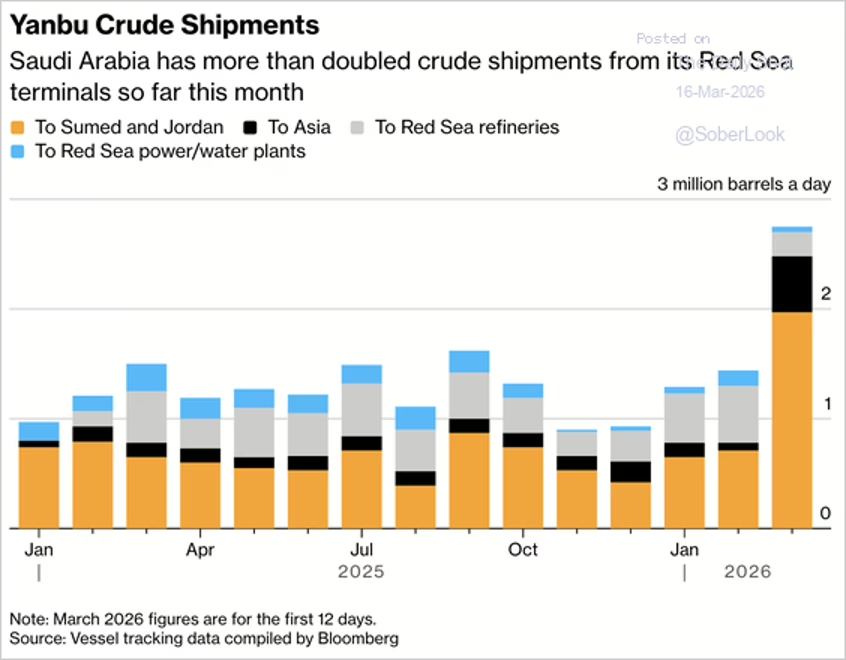

Saudi Arabia is rapidly rerouting crude exports to its Red Sea ports as Riyadh attempts to bypass the Strait of Hormuz, though export flows remain well below the kingdom’s targeted 5 million barrels per day capacity.

Source: @markets Read full article

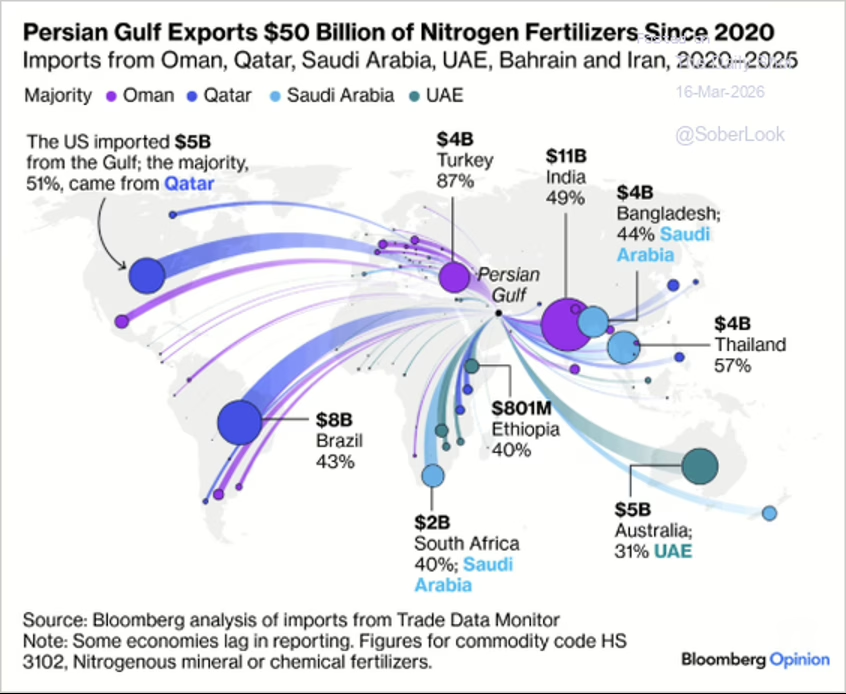

This chart illustrates the flows of nitrogen fertilizers from the Persian Gulf.

Source: Bloomberg via @BlakeMillardCFA

Oil prices eased slightly as Iraq agreed to resume exports via Turkey to avoid the Strait of Hormuz, but Brent crude remains on track to close above $100 for the fifth consecutive session.

AI Effect on the US Economy

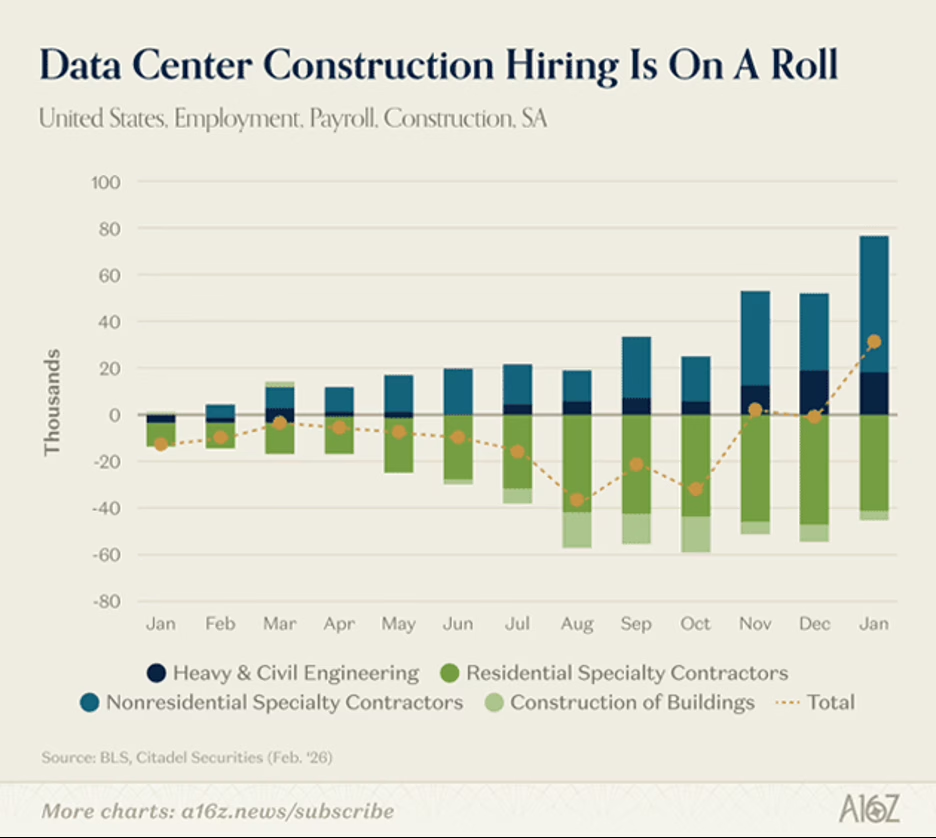

GDP for 2025 was 2%. Peter Boockvar tells us that over half of that was from data center construction. That trend is only going to increase in 2026.

First off, the numbers simply boggle the mind. Just four large technology firms (Amazon, Google, Meta and Microsoft) announced they plan to spend $700 billion in the future on AI infrastructure. This is by itself the largest technology spending in history, dwarfing the dotcom era. And it doesn’t include Anthropic, Grok and a host of other AI firms spending large sums of money but not in that category. And that doesn’t count the literally scores (hundreds?) Of smaller firms bolting onto that infrastructure offering services and apps.

In a recent article, Mckinsey estimates that by 2030, companies will invest almost $7 trillion in capital expenditures on data center infrastructure globally.2 More than $4 trillion of it will go toward computing-hardware investments, with the balance going toward areas such as real estate and power infrastructure (Exhibit 1). More than 40 percent of this spending will be invested in the United States.

My opinion is not all of the current major players will succeed in achieving their goals. That’s what competition is about. But right now, nobody knows who will win. I can guarantee you the boards and management of each of those companies fully intend to be the winner. Further, getting AI right is existential for each of these large companies. If they become the also-ran, their high valuations will collapse and their ability to grow in the future will diminish. It is an arms race and one that they literally cannot afford to lose.

We are seeing a shift in data centers built for training to data centers built for what is called inference. “The cost of training frontier models, while still enormous in absolute terms, has become a smaller fraction of total AI compute spending. The real expense — and the real business opportunity — lies in serving those models to billions of users. Inference now accounts for an estimated 60 to 70 percent of total AI compute demand across major hyperscalers, up from roughly 40 percent in 2024.

“This shift matters for several reasons. Inference workloads have different hardware requirements than training. While training benefits from massive parallel processing across thousands of interconnected GPUs, inference prioritizes low latency, high throughput, and energy efficiency across distributed data centers. This creates openings for specialized inference chips — like Amazon’s Trainium and Inferentia, Google’s TPUs, and dedicated inference accelerators from startups like Groq and Cerebras — to compete with NVIDIA’s dominance in ways that were not feasible in the training-dominated era.” Source: Tech-Insider.org

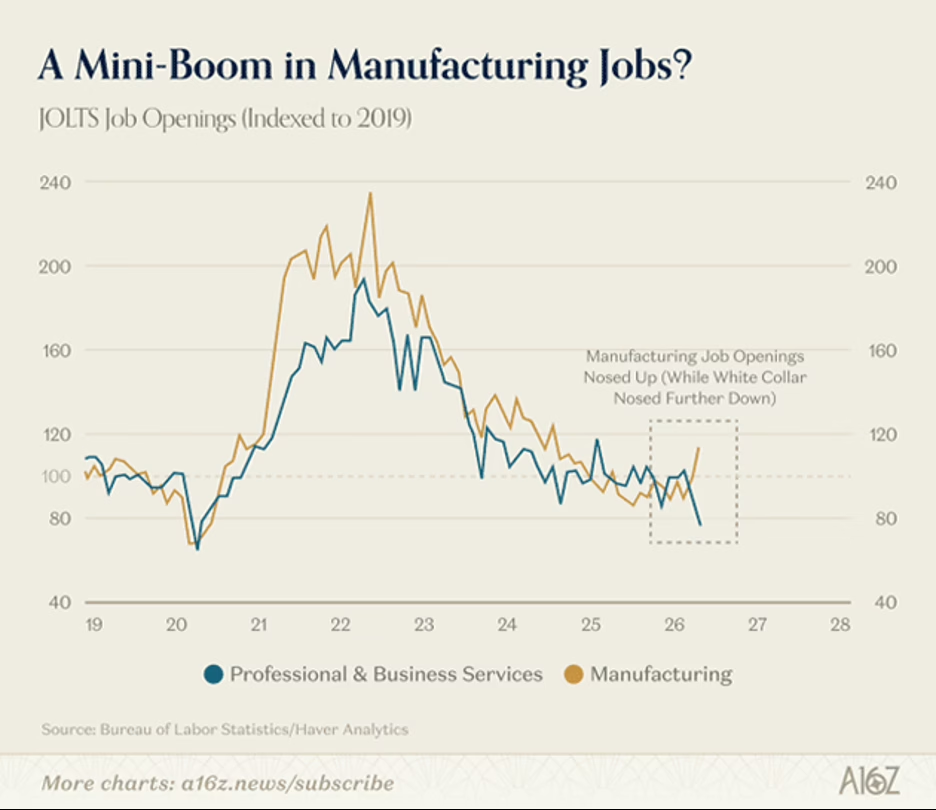

And that translates into jobs. Manufacturing jobs are actually increasing:

This is being powered by data center construction. While regular construction jobs are in decline, those tied to data centers have more than offset the decline.

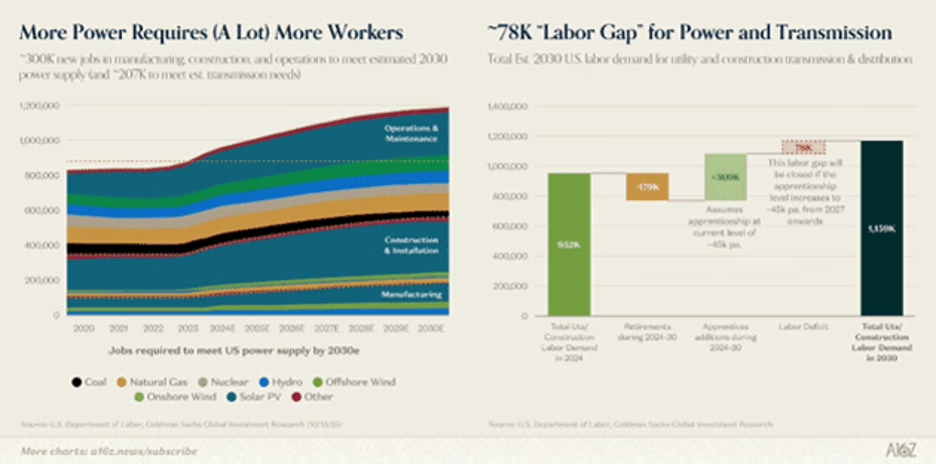

Goldman Sachs estimates that there will be 300,000 new jobs by 2032 just to power the new data centers, and another 207,000 jobs to build out the transmission that will be needed.

As Peter Diamandis notes, “this is beginning to generate serious revenues. $50 billion data centers generating $10 billion annually. $1 trillion in infrastructure deployment. Neuromorphic chips making AI 1,000x more efficient. Fusion energy and small nuclear reactors moving from experiment to grid power. AI is accelerating longevity research. Humanoids going from demos to war zones. SpaceX making orbital access routine.”

We have not experienced anything like this that I can tell in human history. While the advent of the steam engine or electricity or automobiles seriously impacted the economy, it did so over decades. This is happening in years. And that’s not including robotics and other tech related build outs.

Great Quotes

“Negative people. They have a problem for every solution.” – Albert Einstein

Picture of the Week

Second Beach, WA

All content is the opinion of Brian Decker

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}